The Three-Era Fiscal Arc

The New Deal was the most successful redistributive architecture in American history. In the wreckage of the Great Depression, a quarter of the workforce unemployed, banks failing by the hundreds, democracy fracturing at the edges, a set of institutional innovations did something that had never been done at scale in a modern industrial economy. It stabilized a society that was genuinely coming apart. Social Security. Unemployment insurance. The FDIC. The Wagner Act. The regulatory architecture that governed finance for a generation. For thirty years, in combination with the predistributive instruments described in Section II, these institutions produced something genuinely resembling shared prosperity. The extremes of wealth and poverty were narrowed and the middle class expanded. America became a symbol of democracy and the economic engine of the world at a time when totalitarianism and communism were the competing worldviews.23

The problem is not that the New Deal failed. The problem is that it succeeded at a specific task, redistribution, and we have spent seventy years asking it to accomplish a different task its architecture was never designed to perform. Redistribution corrects concentration after it happens. It does not change who participates in ownership before it happens. A Social Security check does not compound and does not appreciate. Medicare pays for care, but does not create a stake in the care enterprise. Unemployment insurance bridges a gap, but does not close it. Every redistributive instrument in the New Deal toolkit is designed for income replacement, not for changing the ownership structure itself. The citizen in the redistributive model remains structurally a recipient.

The New Deal was not a theory. It was triage. When the patient is bleeding, you apply pressure. You do not stop to redesign the circulatory system. But triage is not a long-term health strategy. Redistribution applied across decades as permanent architecture rather than emergency intervention reveals its structural ceiling. You cannot redistribute your way to an ownership society. You can only redistribute your way to a slightly less unequal non-ownership society, and only for as long as the fiscal conditions that make redistribution possible hold.24

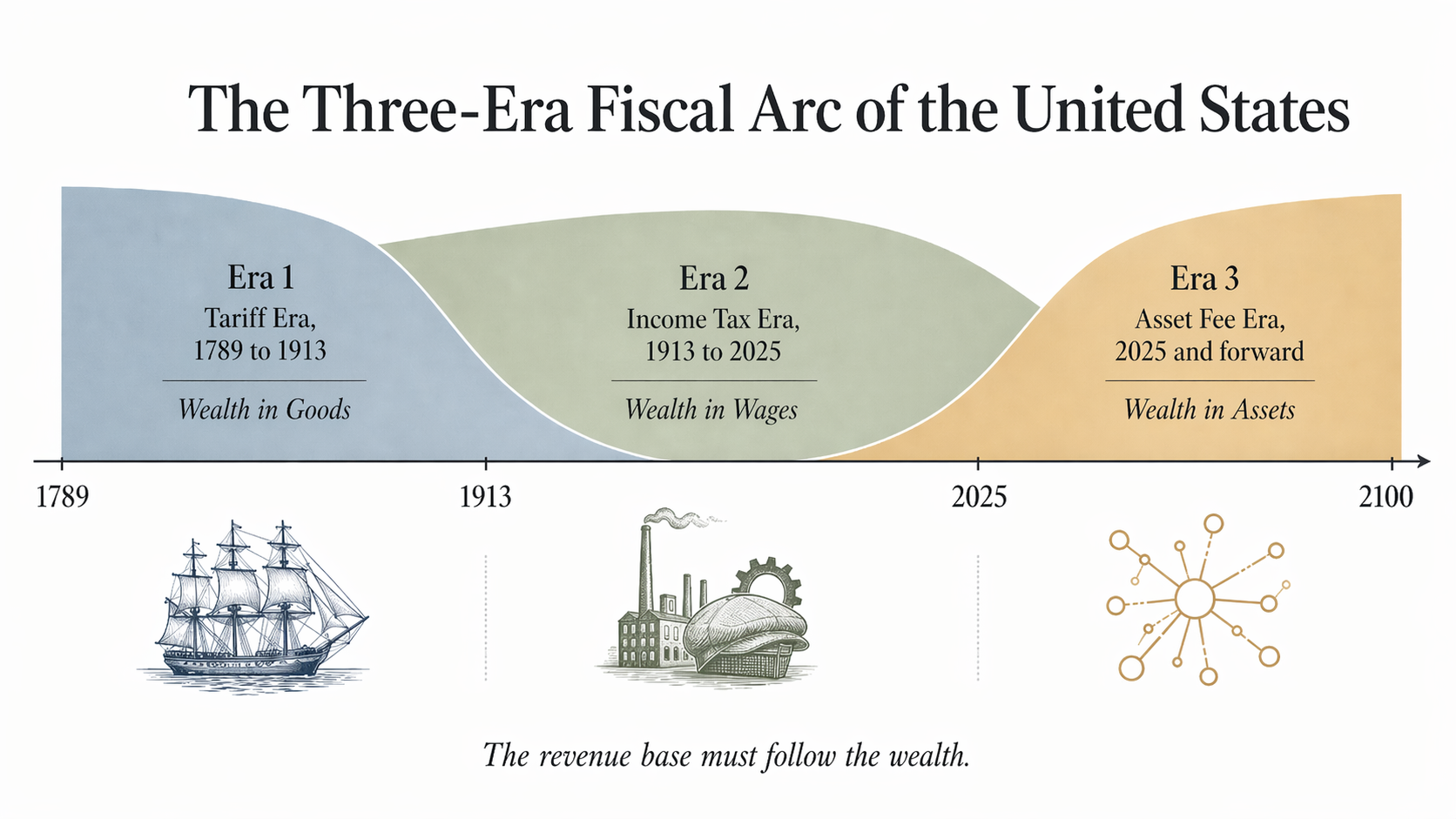

The Three-Era Fiscal Arc

Those conditions are no longer holding. There is a divergence between where the wealth lives and where the revenue base is pointed, and it has been widening for fifty years.

The revenue base of any government must follow the wealth of the economy it governs. The tariff was the principal funding mechanism of the United States for the first 150 years of its existence, because the movement of physical goods in an agrarian and manufacturing economy was the basis of wealth building. When the wealth moved to wages, the revenue base followed. The 16th Amendment established the income tax in 1913, funding the most expansive social insurance system in American history from the wages of a manufacturing, employment-based economy. Both transitions were fought for, contested, and eventually ratified, because the alternative was a government that could no longer govern.

The wealth has moved again. Fifty trillion dollars sit in American retirement accounts alone. The top ten percent of households own seventy percent of all financial assets. The bottom fifty percent own two and a half percent. Corporate equities, real estate, intellectual property, platform infrastructure: the productive capacity of the American economy is organized around ownership now, not around wages. Compounding returns flow to those who hold assets, not to those who sell their labor. And the social insurance system, built on the assumption of a growing wage base, funded by a tax on the thing that is no longer where the wealth primarily lives, faces structural insolvency within a decade.25

This is the Three-Era Fiscal Arc. The tariff era. The income tax era. The Asset Fee Era, which is not coming. It is already beginning, in the form of wealth tax proposals, data levy discussions, AI infrastructure debates, and the growing recognition across the political spectrum that the income tax base cannot sustain the social insurance commitments the country has made. The question is not whether the revenue base shifts toward assets. It will shift. The only question that is actually ours to answer is whether the shift is designed to serve everyone, or designed to serve the people who already hold the assets.

Redistribution applied to the Asset Fee Era produces a larger, more aggressive transfer machine. Better than letting the income tax era collapse without replacement, but insufficient as a permanent architecture, because it does not change the underlying ownership structure. Predistribution applied to the Asset Fee Era produces a different economy: one in which the productive capacity of the asset economy is broadly held before it concentrates, one in which the people who contribute to building the commons hold a stake in what the commons produces, one in which the question of redistribution becomes less urgent because the question of concentration never fully arose.

These are not the same project. They do not produce the same society. The choice between them is being made now, in the decisions of this decade, in the same way the choice between the tariff era and the income tax era was made by a specific generation of legislators, economists, and reformers who recognized that the old revenue base could no longer fund the obligations of the early twentieth century.26 The Asset Fee Era arrives first in one sector, at a scale that forces every other fiscal question into its shadow, and in a form the redistributive architecture was never designed to govern.

Healthcare and the Arithmetic of the Commons

Healthcare is already the largest sector of the American economy. National health expenditures reached $4.9 trillion in 2023, 17.6 percent of GDP, larger than defense, larger than education, larger than any other category of human activity the country records. It is not a vertical alongside other verticals. It is the spine of the social sector, the place where demography, labor, technology, and fiscal policy converge, and the first system in the American economy where the twentieth-century redistributive model arithmetically stops working.27

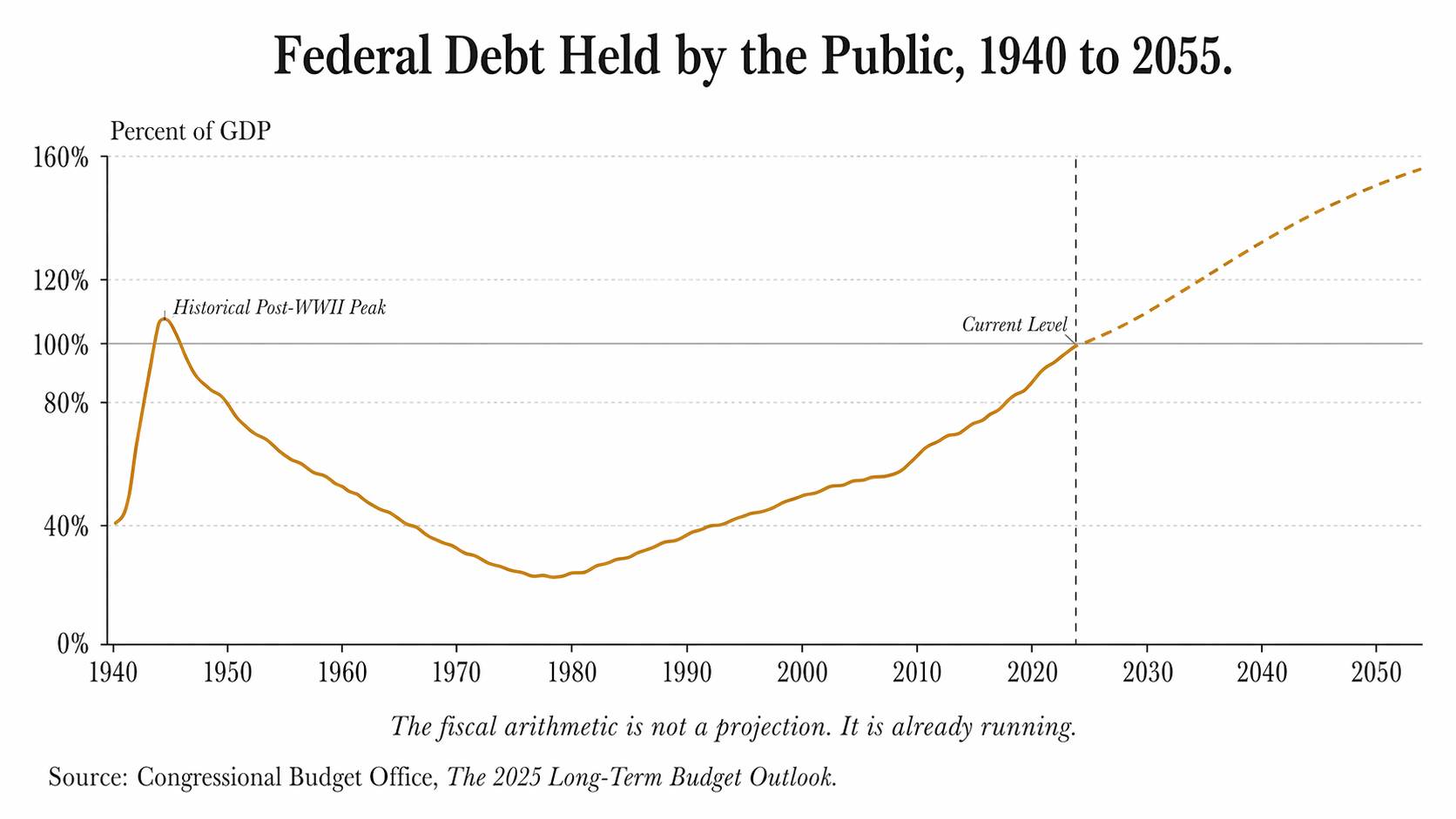

The forces driving that arrival are structural and irreversible. The population is aging. Life expectancy has extended. The old-age dependency ratio, 37 seniors per 100 working-age adults today, rises to 46 per 100 by the 2050s. Care work is labor-intensive, locally delivered, and only partially substitutable by technology. The wage base that funds social insurance is being compressed by AI and automation in the sectors where labor can be replaced, even as demand rises fastest in the one sector where it cannot. The fiscal arithmetic follows directly. Federal debt held by the public is roughly 100 percent of GDP today. Under current law, by 2055 it reaches 156 percent, driven by the compounding interaction of an aging population, healthcare cost growth above general inflation, and interest payments on existing debt. Spending on Social Security, major federal health programs, and net interest rises from 14.2 percent of GDP in 2025 to 19.6 percent by 2055, while revenues rise only 2.2 points over the same period. The gap between those trajectories is not a projection. It is a design mismatch. The system is not failing because it is mismanaged. It is failing because it is correctly designed for conditions that no longer exist.28

This is why redistribution alone cannot close the gap. Healthcare is where the old model breaks first because it is where demographic inversion, labor that resists automation, and a shrinking tax base compressed by automation everywhere else converge in the same sector at the same time. AI substitutes for cognitive labor. Robotics substitutes for physical labor. Together they compress the wage base that funded the twentieth-century social contract from both ends simultaneously, and the arithmetic of that compression is no longer a projection. It is the trajectory the capital has already chosen.29

The revenue base must follow the wealth, into assets, into data, into the returns from the infrastructure that increasingly produces the economy's output, because the wage base it used to follow is no longer where the wealth lives.

The Compounding Logic and Who It Serves

The compounding logic at the center of the American economic engine is the structural answer to this convergence, the mechanism by which contribution, held patiently over time, builds the stake that no redistributive transfer ever can. It is also the oldest argument in the American economy, made repeatedly across three generations of practitioners and thinkers who arrived at the same structural conclusion from different directions: Kelso from first principles, Buffett from six decades of practice, Thiel from the architecture of platform monopoly. The mechanism works. It has always worked. The only question left is who it works for.

Louis Kelso saw it first, in 1958, not from historical data but from the internal logic of capitalism itself. If capital ownership decisively overtakes wage labor as the primary driver of wealth creation, he argued, the solution is not higher wages or redistribution but broader ownership, making the mechanism that compounds work for more people, not just the people who already hold assets. His invention, the Employee Stock Ownership Plan, was the first systematic American mechanism for converting labor contribution into ownership stake before the profits are generated rather than distributing income after the fact. It worked. There are thousands of ESOP companies in the United States, and they are on average more productive, more stable, and more equitable than their conventionally owned counterparts. The mechanism was real. But the ESOP has a ceiling that Kelso's century could not see past. It was designed for the industrial economy, for a world where the contributor is an employee, the enterprise is a firm with identifiable physical assets, and the ownership stake can be formalized within the structure of employment. The knowledge economy breaks all three conditions. The teacher whose thirty years of curriculum innovation is absorbed into an AI training set is not an employee of the company that trained the model. The care worker whose institutional knowledge is the actual product of the care relationship owns nothing of the enterprise that depends on her staying. The ESOP is the right answer applied to the wrong century. It pointed toward the principle without being able to complete it.30

Warren Buffett proved the principle at a scale Kelso never reached. Over six decades, through patient long-term investment in productive enterprises with genuine competitive advantages, businesses with durable moats, honest management, and predictable earnings, Berkshire Hathaway compounded capital at a rate that made it one of the most valuable enterprises in human history. The mechanism was not financial engineering. It was not speculation or extraction. It was ownership, held patiently, allowed to compound, trusted to generate returns over decades rather than quarters. Buffett demonstrated that the compounding logic of capital, applied with discipline and time, is the most powerful wealth-generating mechanism available, more powerful than wages, more powerful than redistribution, more powerful than any income-based strategy ever devised.

He also said something almost no one at his level of the ownership economy has been willing to say plainly: that he won what he called the ovarian lottery. Being born in America, in this century, with his particular aptitudes, in a system that rewards those aptitudes, accounts for the overwhelming majority of what he has accumulated. He has called the American institutional infrastructure, the rule of law, the financial architecture, the educated workforce, the social trust, the American Tailwind, and he has acknowledged that without it, his compounding logic would have had nothing to compound on. The argument of this Declaration is that Buffett is right about everything. Right about the power of the compounding mechanism. Right about the Tailwind that makes it possible. Right about the extraordinary productive capacity of the American economic engine. And he has not yet followed his own acknowledgment to its structural conclusion: that the Tailwind is a commons, that the commons requires governance, and that the people whose labor, care, and civic participation maintains it deserve the same compounding ownership stake that Buffett has spent his career building for those who arrived with capital.31

Buffett proved that the compounding mechanism, applied with patience and structural discipline, generates more durable value than any alternative. He left open the question of who owns the architecture that makes compounding possible. Thiel answered that question with uncomfortable precision.

Zero to One is, on its surface, a defense of corporate power. It is actually a theory of how transformative value gets created and how it compounds. Thiel argues that the goal of any serious builder is not to compete better but to escape competition entirely by creating something categorically new, and that durable value comes from building four characteristics into the foundation: proprietary technology that is qualitatively superior, network effects that compound with each additional user, economies of scale that drive marginal cost toward zero, and brand that makes alternatives feel wrong rather than merely inferior. The founding moment is the moment of maximum leverage, because the architectural decisions made at the founding determine the ceiling of what is possible for the life of the platform. Change the architecture later, and you are fighting the compounding you already set in motion.

The Declaration accepts Thiel's analysis of how compounding works entirely. The disagreement is not about the mechanism. It is about the ownership of the mechanism. The commons of human knowledge, care, relationship, and culture already has all four of Thiel's characteristics. It has proprietary depth that no competitor can replicate, three hundred thousand years of accumulated human thought. It has network effects, every additional contributor making it richer for every existing contributor. It has economies of scale, with the marginal cost of an additional person drawing on the shared intellectual and relational infrastructure approaching zero. And it has the deepest brand possible: it is the foundation of everything human civilization has ever built. What Google, Facebook, and the AI companies have done is precisely what Thiel prescribes: identify the most valuable unbuilt position, establish architectural dominance before competitors understand what is being built, and design the four characteristics into the foundation so the position compounds indefinitely. They did it correctly. What they built their monopoly on was the commons, and they built it so the compounding flows upward to the owners of the architecture rather than outward to the contributors who made it possible.

and they built it so the compounding flows upward

to the owners of the architecture

rather than outward to the contributors who made it possible.

The same architectural discipline, applied from the beginning with ownership designed to compound outward rather than upward, produces a different economy. Not because contributors are more virtuous than capital holders, but because the architecture can be designed that way, and once designed that way, it compounds that way for the life of the platform. You cannot monopolize abundance if abundance is the product of relationship. The architecture that captures relational and intellectual abundance must compound outward, which is not a departure from Thiel's logic but its completion, applied to a commons rather than a corporation.32

Predistribution in 2026

The instruments of 1945 are not the instruments of 2026. The GI Bill worked because a specific population, sixteen million returning veterans, met a specific asset class, housing in a specific window of appreciation, through a specific institutional infrastructure, the FHA, the VA, and the university system that could deliver the stake at scale before the post-war wealth concentrated. Those conditions are gone and the instruments must change, but the principle still holds.

Predistribution in 2026 looks like a care cooperative where workers earn ownership stakes in the enterprise their labor builds. It looks like a public semiconductor strategy where the public investment creates a public equity stake held in community wealth funds rather than dissolved into private balance sheets. It looks like an AI governance framework where the training data commons generates a collective ownership stake for the communities whose knowledge made the model possible, held in a structure that cannot be revoked when the political coalition changes or the corporate strategy shifts. Redistribution asks who gets the proceeds. Predistribution asks who owns the thing that produces them.33 Predistribution is a direction, not a blueprint. What follows is the set of principles that any architecture pointed in that direction must satisfy.

Predistribution asks who owns the thing that produces them.