The Shifts

In post-war America, from roughly 1945 to 1975, the American economy did something it had never done before and has not done since: it distributed the gains of growth broadly enough that a working family sustained by wages could build genuine security across a generation. Wages rose alongside productivity. Labor's share of national income held between 60 and 65 percent of GDP for thirty years. The middle class expanded not as a cultural aspiration but as a structural fact. The American Dream, for that specific window, was measurably achieved.

The conditions that produced broad prosperity were specific and deliberate, not natural or self-sustaining. Understand the architecture and you understand both what made it possible and why it cannot simply be restored.

The Geopolitical Accident

The first condition was unrepeatable, because the United States emerged from World War II as the only fully intact industrial economy on earth. Europe and Japan lay in ruins. The Soviet Union had lost twenty million people and vast productive capacity. Every other major industrial power was rebuilding from near-zero while American cities stood unburned, American factories ran at full capacity, and American supply chains were intact. We had nuclear supremacy and control of the world's oceans. We had written the rules of the new global order including the IMF, the World Bank, Bretton Woods, and the dollar as the world's reserve currency. For thirty years, American workers shared in a prosperity that was partly the product of deliberate structural choices and partly the product of having no serious competition.

That geopolitical accident is not reproducible. China, Germany, South Korea, Japan, the Middle East; the global economy is now genuinely multipolar in ways it was not between 1945 and 1975. Any argument for rebuilding broad prosperity that depends on American economic dominance of the kind that existed in those decades is not a structural argument. It is a wish.

What can be reproduced are the structural choices that converted geopolitical advantage into broadly distributed ownership rather than concentrated wealth. Those choices were not inevitable. They were fought for, legislated, and maintained against determined opposition. And they worked on a principle that is available to any economy in any era, regardless of geopolitical position: predistribution.

The Predistributive Architecture

Predistribution means embedding broad ownership into the structure before wealth concentrates, before the asset class forms, before the rules of the game are written by the people who already won. The post-war generation did not use this word. They were responding to a crisis, to the living memory of the Depression, to the social contract forged in wartime. But the instruments they built were predistributive in their structure, whatever their designers called them.

The GI Bill was the most consequential. Sixteen million returning veterans were distributed into the asset economy at a moment before the post-war wealth had fully accumulated. Education benefits, low-interest mortgages, business loans were the transition from a wartime economy, and the entry point into broad ownership of productivity gains in the decades to come. A veteran who used the GI Bill to buy a house in 1948 participated in thirty years of appreciation that funded his children's education, served as collateral for whatever he built next, and transferred to the following generation as a head start that compounded again. He did not receive a one-time wealth transfer, or welfare; he received a stake in the American Dream.

FHA mortgage guarantees turned renters into owners at scale, creating the suburban middle class as a structural reality rather than an aspiration. The mechanism was not redistribution of existing wealth but the creation of new asset-holders before the post-war wealth had concentrated. Union membership at its peak, over 35 percent of the private workforce by the mid-1950s, gave workers genuine bargaining power not just over wages but over the share of productivity growth that would flow to labor rather than to capital. Marginal tax rates above 90 percent for the highest earners made it structurally irrational to hoard wealth at the top rather than reinvest in wages and productive capacity. The Glass-Steagall Act passed in the 1930s directed capital toward productive investment rather than financial speculation.

Every one of these instruments was fought for against determined opposition. The business community resisted union power at every step. The financial industry chafed against regulation. None of it was natural. All of it was designed. And the design worked, for the specific population it included, precisely because it was predistributive. The result was a generation of genuine asset-builders rather than wage-earners watching prosperity compound upward without them.

The word that names what the post-war architects built without knowing they were building it is also the word that names what the New Deal could not fully deliver and what the shareholder revolution of the 1970s deliberately dismantled: ownership stakes in productive assets. By 1991, academic Michael Sherraden identified this as the structural challenge the New Deal fails to account for: income supports consumption; assets enable investment, stability, and mobility across generations. The welfare system's exclusive focus on income maintenance was not a partial solution to poverty. It was a system designed to manage poverty rather than end it, because it addressed the output of the ownership gap without touching the ownership gap itself.4

before wealth concentrates.

The Architecture of Exclusion

The post-war prosperity was real. It was also structurally bounded by design.

The GI Bill applied on paper to all veterans. In practice its wealth-building mechanisms were systematically withheld from Black veterans through a combination of legal architecture and deliberate administration. The Veterans Administration delegated implementation to local institutions which refused mortgage loans to Black applicants. The best-funded universities were segregated. The suburban developments built through FHA mortgage guarantees carried explicit racial covenants enforced by the federal government itself: the FHA's own underwriting manual rated neighborhoods with Black residents as high-risk and required racial homogeneity as a condition of loan guarantee. This was not private discrimination the government failed to prevent. It was discrimination the government designed and administered.

The structural consequence was not merely that Black families missed the post-war boom. It is that they were excluded from the mechanism by which the post-war boom compounded. A white working-class family that bought a house in a guaranteed suburb in 1948 did not simply enjoy prosperity in that decade. They participated in thirty, forty, fifty years of appreciation — equity that funded college tuitions, served as collateral for business loans, and transferred to the next generation as a head start that compounded again. Three generations of that compounding is what the wealth gap between white and Black households in America actually measures today. It is not primarily a wage phenomenon. It is not a cultural phenomenon. It is a compound interest problem, the direct output of a structural decision made in 1945 and running forward, uninterrupted, ever since.5

Post-war architecture proved that predistribution works and broad ownership distributed before concentration produces genuine and durable prosperity. It also proved that predistribution works only as broadly as the circle of inclusion is drawn. When the circle is deliberately narrowed, the mechanism still operates, it just operates for fewer people, and the exclusion compounds alongside the prosperity. The next architecture must draw the circle differently, not as an act of contrition but as the structural correction that honest accounting demands. An architecture that excludes by design is an architecture that reproduces the problem it claims to have solved.

The Break

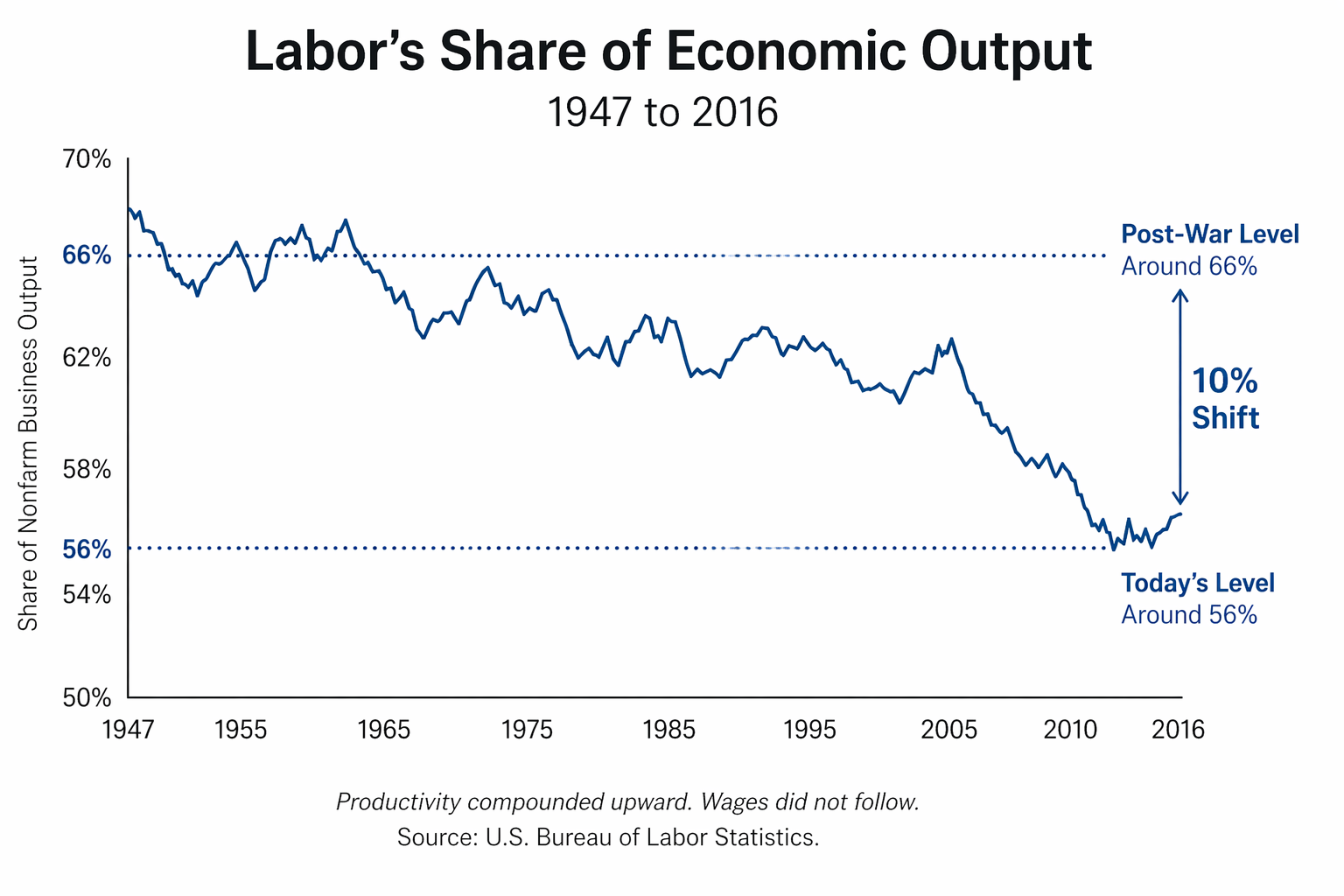

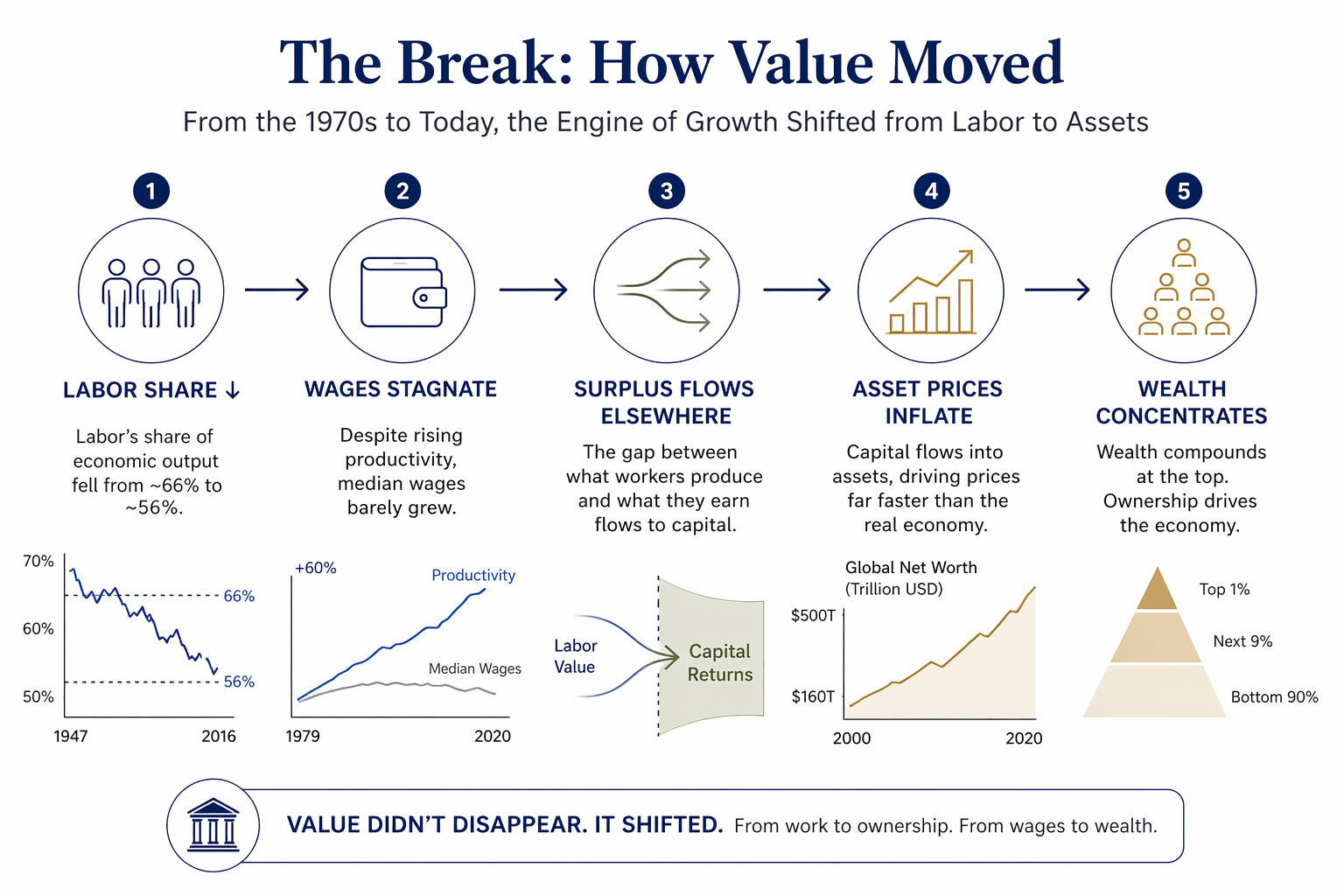

Productivity and wages, which had moved together for thirty years, diverged in the early 1970s and never reconverged. Productivity kept rising. Wages did not. The value that workers produced continued to compound, but it no longer compounded into paychecks. It compounded upward, into asset values, into equity, into returns on capital rather than returns on labor. Since 1979, productivity in the United States has risen by more than 60 percent. Median wages have risen by roughly 17 percent. The difference did not disappear. It was redirected.

That redirection is visible in a single shift. In the post-war decades, labor received roughly two-thirds of the value the economy produced. Today, it receives closer to three-fifths. That ten-point shift is not abstract. It represents trillions of dollars per year moving away from wages and toward profits, capital returns, and asset holders. What workers lost as income did not vanish. It accumulated elsewhere.

For decades, that shift could be debated. Today, it can be measured directly. Between 2000 and 2020, global net worth increased from $160 trillion to over $500 trillion, while global GDP grew far more slowly. The world did not produce three times more goods and services. Instead, the value of what already existed, homes, land, equities, financial assets, was repriced upward. Nearly 80 percent of that increase came not from new investment but from rising asset prices.

And the people who benefited are a narrow slice of the population. In the United States, the top 10 percent of households owned 71 percent of the nation's wealth by 2019, up from 67 percent in 2000. The bottom 50 percent owned 1.5 percent, down from 1.8 percent. Asset inflation is not broadly distributed prosperity. It is a transfer mechanism from those who hold assets to those who hold more of them, with roughly half the population holding almost nothing that appreciates.

This is the missing link. The stagnation of wages and the explosion of wealth are not separate phenomena. They are the same phenomenon viewed from opposite sides of the balance sheet. When labor's share declines, the surplus does not disappear. It flows into profits. When profits accumulate, they are reinvested into assets. When capital chases assets faster than the real economy grows, asset prices rise. And when asset prices rise, wealth concentrates in the hands of those who already own them. This is not a distortion of the system. It is the system operating as designed.7

By the early 1970s, the post-war architecture was under strain. Stagflation exposed the limits of Keynesian demand management. Regulated industries had become inefficient and captured by insiders. Unions, at their worst, protected incumbents without delivering corresponding productivity. The critique that incentives matter, that capital must be allowed to move, that markets allocate resources more efficiently than rigid systems, was not wrong. What followed, however, was not a recalibration. It was a reorientation of the system's objective function.

Milton Friedman's 1970 declaration that the sole responsibility of business is to increase shareholder value was not a description. It was an instruction. Corporate America followed it with precision. Returns to capital became the organizing principle of the economy. Reagan's dismissal of the air traffic controllers in 1981 signaled that labor would no longer have institutional protection at the highest level, and union membership began a decline from which it has never recovered. Financial deregulation, culminating in the repeal of Glass-Steagall, redirected capital away from productive investment and toward financial assets. Finance expanded from a supporting function into a dominant sector, growing from roughly 2.5 percent of GDP in 1945 to more than 8 percent by 2020.8

These changes did not fail. They succeeded on their own terms. Capital became more mobile. Markets became more efficient. Technology advanced rapidly. The problem is that the system that replaced the post-war model had no mechanism to distribute ownership alongside participation. Thomas Piketty formalized the result mathematically: when the rate of return on capital exceeds the rate of economic growth, wealth concentrates. The post-war period suppressed that dynamic through a specific set of institutions, strong labor participation, progressive taxation, regulated capital flows, and broad-based access to ownership. When those structures were removed, the underlying arithmetic reasserted itself.9

This is why wages are not coming back. Wages are tied to labor. Labor is no longer the primary driver of value capture. Ownership is. As long as the system channels gains into assets rather than income, growth will continue to show up in balance sheets, not paychecks. The economy can expand, technology can advance, productivity can rise, and the distribution mechanism will still channel the gains upward. Social insurance systems funded by taxes on wages, in an economy where wealth has migrated decisively to assets, face an arithmetic they cannot solve. As the population ages and the ratio of workers to retirees declines, that mismatch becomes unsustainable. The system was designed for a wage economy. It is now operating inside an asset economy.

The break is not that growth stopped. It is that growth changed form. And until ownership is addressed directly, the results will continue to concentrate, no matter how much the economy produces.

It is that growth changed form.

The 80-Year Cycle

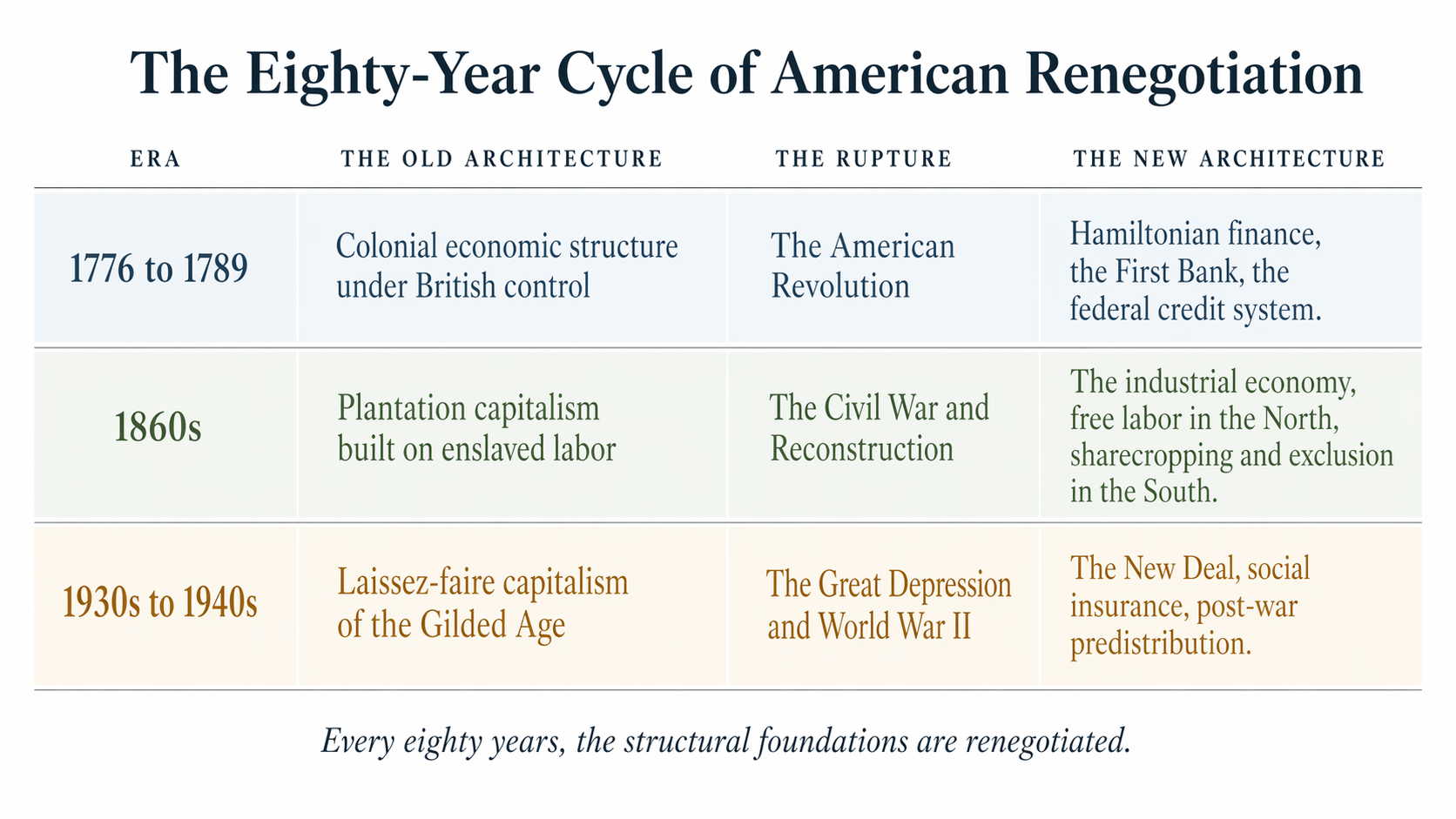

Every eighty years, roughly, the structural foundations of American capitalism are renegotiated. The basic terms of who owns what, who governs the mechanisms of wealth creation, and on whose behalf the economy is organized are renegotiated at the foundation.

1776 to 1789: the Revolution broke the colonial economic structure. Hamilton's architecture replaced it. A new nation, a new financial system, new terms for who could participate in the economy and under what conditions.

The 1860s: the Civil War destroyed the plantation economy, the foundational structure of American capitalism in the South, the system that had made both North and South wealthy on the labor of people it treated as property. The Reconstruction amendments attempted, however incompletely and however brutally suppressed, to rewrite the terms of participation for four million people who had been held as capital rather than recognized as contributors. That attempt failed. The architecture that replaced it was sharecropping, convict leasing, the systematic exclusion of Black Americans from the wealth-building mechanisms of the industrial economy. It was a renegotiation in the wrong direction. But the old architecture could not survive the contradiction that had destroyed it, and from those ruins the United States built the largest industrial economy the world had yet seen.

The 1930s and 1940s: the Great Depression demolished the laissez-faire consensus of the Gilded Age. The New Deal rewrote the basic relationship between the federal government, capital, and labor. Then came the war, and from it the post-war architecture described above, the thirty-year window when the predistributive instruments briefly held and the American Dream was measurably within reach of working people.

It changes either way.

The question is who is in the room when it does.

We are eighty years from the New Deal. Wages have decoupled from productivity for fifty years, the institutions built to redistribute opportunity are fiscally strained and politically contested, and the Social Security Trust Fund faces structural insolvency within a decade. The revenue model of our social safety net was designed for a demographic pyramid that no longer exists, funded by a wage base that no longer captures where the wealth lives. Addressing today's challenges with yesterday's approach is the reason for our deepening political divisions: we are pointing fingers at one another instead of looking at the structures that can no longer serve their purpose. Artificial intelligence is compressing the timeline further, concentrating economic power at a speed and scale the old architecture was never built to govern. The question is not whether the architecture changes. It changes either way. The question is who is in the room when it does.