A Declaration of Interdependence

The Founding Gap

The Declaration of Independence is one of the most extraordinary political documents ever written. Its second sentence announces, with the confidence of a self-evident truth, that all men are created equal, endowed with unalienable rights to life, liberty, and the pursuit of happiness. Governments exist to secure these rights. When they fail, the people may alter or abolish them. In 1776, that sentence was an act of intellectual courage and political audacity that changed the trajectory of human history. It is also, from the beginning, incomplete.

The men who signed it held other men in bondage, an economic structural condition that the political contradiction has never been able to fully reckon with. The Declaration is incomplete because it articulates a vision of political equality without addressing the economic architecture on which political equality depends. It tells us that people are equal before the law. It does not tell us how wealth will be organized, how productive assets will be governed, or how economic power will be constrained. It declares the destination without describing the road.

That gap between the political promise and the economic structure is the space in which the entire American experiment has been unfolding ever since. Every major conflict in American political life, from the battles over the First Bank to the Civil War to the New Deal to the platform economy of the digital age, has been an argument about what that gap contains and whether it can be closed. The argument has never been resolved. It has only been deferred from one generation to the next at compounding cost.

This Declaration is the attempt, in the 250th year of the experiment, to finally name what the first one left out.

The Founding Disagreement

Two figures define the founding tension with unusual precision, because they articulate its poles with the clarity that comes from genuine intellectual seriousness and genuine disagreement about what the world requires. Jefferson and Hamilton are typically presented as rivals, and while that framing is accurate, it is also insufficient. They were not merely political opponents competing for influence in Washington's cabinet. They were expressions of two fundamentally different theories of what freedom requires, what it means for a system to fail, and they arrived at different conclusions about what architecture a republic needs to survive.

Jefferson's theory emerges from abundance and stability. Born into the Virginia gentry, he inhabited a world in which economic independence already exists. The independent farmer, working his own land, answerable to no distant institution, is for Jefferson the citizen in his ideal form: free because he is not economically dependent on others, capable of self-governance because no one holds his livelihood in their hands. In this vision, concentrated power is the danger. It creates dependency. It distances decision-making from the people most affected by its consequences. The task of political economy is restraint, keeping power from concentrating in any single hand, keeping institutions from growing so large that they escape democratic accountability. Freedom, in Jefferson's framework, is the absence of domination.

But the historian Richard Hofstadter identifies something deeper in Jefferson than mere anti-centralism: a consistent pattern of temporal deferral. Jefferson articulates universal principles and places their realization in the future, in the gradual unfolding of history, rather than in the immediate transformation of structures. He believes in equality as an abstract truth but declines to translate it into decisive structural action, explaining, in the case of slavery, that "the public mind would not bear it." This is a template the American political tradition has reproduced across two centuries: expansive principles articulated, structural implications deferred, the gap managed rather than closed.1

Hamilton's theory emerges from the failure and collapse of Valley Forge, in the darkest hours of the American Revolution. He comes of age not in the stability of a Virginia plantation but inside Washington's command during the Revolution, watching a system that cannot function. Men wrapping their feet in rags because there are no boots. States refusing to cooperate because there is no central authority that can compel them. A treasury empty and a war that might be lost not because the cause is wrong, but because the structure is defective. From this experience Hamilton draws a conclusion that defines the rest of his life: fragmented power is as dangerous as concentrated power. A system that cannot act is not free. It is vulnerable. The task of political economy is not restraint but designing the institutions, the financial architecture, the mechanisms of collective action that allow a republic to survive contact with reality. Freedom, in Hamilton's framework, requires infrastructure.

These are not minor differences in policy preference. They are opposing answers to the same question: what does it actually take for a society to remain free? Neither is sufficient alone. Concentrated power dominates. Fragmented power collapses. The American system is built, and has always been rebuilt, in the tension between these truths.

But here is what the standard telling misses, and what matters most for the argument this Declaration makes: the system operates Hamiltonianly. It justifies itself Jeffersonianly.

Hamilton gave it its bones.

The United States, despite its rhetorical attachment to individual independence and suspicion of concentrated authority, has developed along unmistakably Hamiltonian lines. National markets, a central bank, federal investment in infrastructure and technology, the most powerful financial system in human history are all organized by institutions Hamilton would recognize as the direct descendants of his original architecture. At the same time, the language through which this system is understood and defended remains deeply Jeffersonian: freedom as individual self-reliance, government as the obstacle rather than the instrument, markets as self-regulating mechanisms that need only to be left alone. The result is an economy that concentrates through Hamiltonian structures while telling a Jeffersonian story about why the concentration is natural and just.

And beneath both stories runs a consensus that neither Hamilton nor Jefferson fully questioned: that the architecture of property and ownership is essentially fixed, that the task of political economy is to govern it, restrain it, or harness it, but not to redesign who participates in it.2 That unquestioned consensus is the founding gap this Declaration is written to close.

What Hamilton Understood

Capital is not money. It is a transformative mechanism that converts fixed assets into productive resources that compound over time. Land without legal title is an asset. Land with clear title, recorded in a public registry, eligible for use as collateral is capital. The same physical thing. A completely different economic function. The difference is not in the thing itself. It is in the structure that surrounds it.

Hamilton understood that the United States in 1789 was not poor in resources. It was poor in the institutional infrastructure that could convert those resources into productive national power. His genius was to build that infrastructure at a national scale and to build it in such a way that the people with the most to gain from its failure had, instead, a financial stake in its survival. By assuming the war debts of all thirteen states and converting them into federally backed obligations, he created a class of creditors whose personal financial interests were now tied to the republic's survival. He did not appeal to their patriotism. He made it rational for them to act as though they had it. The mechanism was debt. The result was interdependence; structured, incentivized, and durable precisely because it did not depend on anyone being virtuous.

That principle, give people a genuine stake in what is being built, and they will help build it is the founding insight this Declaration extends. Not Hamilton's specific instruments. The principle beneath them, which has never stopped being true: freedom requires architecture, and architecture requires that the people who contribute to what is being built have a real stake in what it produces.

The Hamilton beloved by Wall Street, the champion of concentrated finance, the skeptic of mass democracy is a selective portrait. The Hamilton who actually existed, believed that concentrated private power, left ungoverned, was as dangerous as a tyrannical state. His most important move was a governance insight disguised as a financial policy. His design for the First Bank of the United States was a hybrid institution, neither purely public nor purely private, whose purpose was not to maximize profit but to serve what he called public utility. Private participation was essential, but it was embedded within a framework that subordinated individual gain to systemic function. He did not simply unleash markets. He organized them toward collective ends. Ideals inspire. Structures sustain.

His mechanism solved the political problem of 1789: how to make it rational for the wealthy to support public institutions. What it did not solve is the inversion of that question. Not: how do we make it rational for the wealthy to support the republic? But: how do we ensure that the people whose labor, care, knowledge, and contribution actually build the republic hold a genuine stake in what it produces?

Hamilton tied the creditors to the nation through debt. His legacy lies in his recognition that freedom in a complex society is not simply the absence of constraint but the presence of capacity. Independence understood as isolation from systems is insufficient. What is required is the ability to act effectively within them, and that requires institutions, coordination, and design. An architecture of power. Hamilton built the first version of that architecture for the creditors of the new republic. The argument this Declaration makes is that the same principle, pointed in a different direction, must now be built for the people whose labor, care, and knowledge have always been the foundation of what the architecture produces.3

His legacy lies in his recognition that freedom in a complex society

is not simply the absence of constraint but the presence of capacity.

The Sentence That Was Left Unfinished

The Declaration of Independence declared political equality and left the economic question open. That was not, in the context of 1776, a failure of courage or vision. It was the limit of what was politically achievable in a coalition that included Virginia planters and Massachusetts merchants, abolitionists and slaveholders who needed one another to win a revolution and could not yet agree on what came after.

The economic question was deferred. And deferral, in structural matters, is not neutral. Deferral compounds. Every generation that did not answer the question passed the cost of not answering it to the next generation, at compound interest, until the gap between the founding promise and the lived reality of most Americans became the defining fact of political life.

We are now eighty years from the last moment the question was seriously engaged, during the New Deal and the post-war architecture that followed. That architecture stabilized American democracy through the middle of the twentieth century and has now reached its structural limits. The question 1776 opened is the question this generation must answer, not because the moment is comfortable or the conditions are ready, but because the pattern of deferral has finally run out of road. The decisions being made in this window will compound across generations the way the decisions of 1776 and 1789 compounded across the generations that followed.

The Shifts

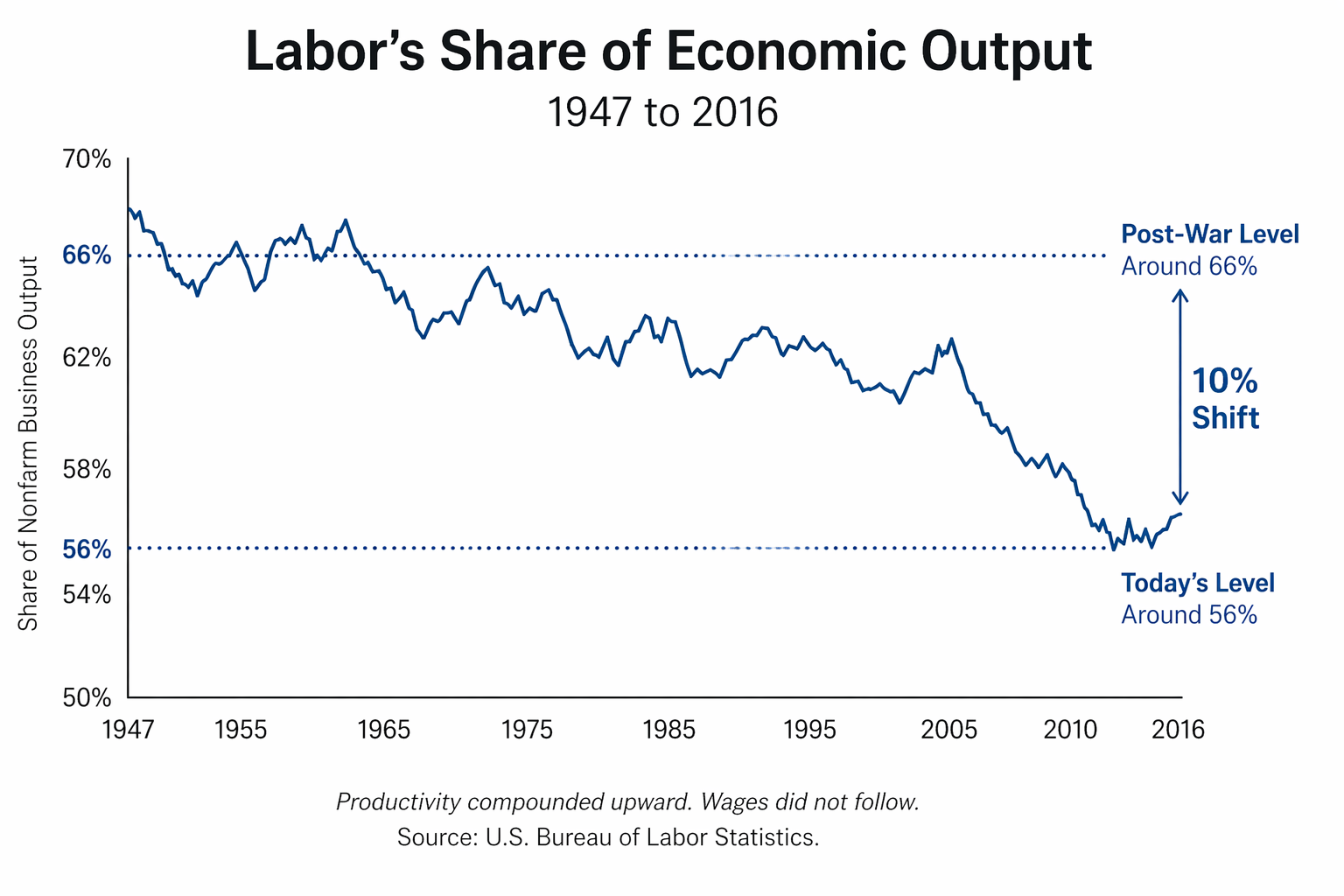

In post-war America, from roughly 1945 to 1975, the American economy did something it had never done before and has not done since: it distributed the gains of growth broadly enough that a working family sustained by wages could build genuine security across a generation. Wages rose alongside productivity. Labor's share of national income held between 60 and 65 percent of GDP for thirty years. The middle class expanded not as a cultural aspiration but as a structural fact. The American Dream, for that specific window, was measurably achieved.

The conditions that produced broad prosperity were specific and deliberate, not natural or self-sustaining. Understand the architecture and you understand both what made it possible and why it cannot simply be restored.

The Geopolitical Accident

The first condition was unrepeatable, because the United States emerged from World War II as the only fully intact industrial economy on earth. Europe and Japan lay in ruins. The Soviet Union had lost twenty million people and vast productive capacity. Every other major industrial power was rebuilding from near-zero while American cities stood unburned, American factories ran at full capacity, and American supply chains were intact. We had nuclear supremacy and control of the world's oceans. We had written the rules of the new global order including the IMF, the World Bank, Bretton Woods, and the dollar as the world's reserve currency. For thirty years, American workers shared in a prosperity that was partly the product of deliberate structural choices and partly the product of having no serious competition.

That geopolitical accident is not reproducible. China, Germany, South Korea, Japan, the Middle East; the global economy is now genuinely multipolar in ways it was not between 1945 and 1975. Any argument for rebuilding broad prosperity that depends on American economic dominance of the kind that existed in those decades is not a structural argument. It is a wish.

What can be reproduced are the structural choices that converted geopolitical advantage into broadly distributed ownership rather than concentrated wealth. Those choices were not inevitable. They were fought for, legislated, and maintained against determined opposition. And they worked on a principle that is available to any economy in any era, regardless of geopolitical position: predistribution.

The Predistributive Architecture

Predistribution means embedding broad ownership into the structure before wealth concentrates, before the asset class forms, before the rules of the game are written by the people who already won. The post-war generation did not use this word. They were responding to a crisis, to the living memory of the Depression, to the social contract forged in wartime. But the instruments they built were predistributive in their structure, whatever their designers called them.

The GI Bill was the most consequential. Sixteen million returning veterans were distributed into the asset economy at a moment before the post-war wealth had fully accumulated. Education benefits, low-interest mortgages, business loans were the transition from a wartime economy, and the entry point into broad ownership of productivity gains in the decades to come. A veteran who used the GI Bill to buy a house in 1948 participated in thirty years of appreciation that funded his children's education, served as collateral for whatever he built next, and transferred to the following generation as a head start that compounded again. He did not receive a one-time wealth transfer, or welfare; he received a stake in the American Dream.

FHA mortgage guarantees turned renters into owners at scale, creating the suburban middle class as a structural reality rather than an aspiration. The mechanism was not redistribution of existing wealth but the creation of new asset-holders before the post-war wealth had concentrated. Union membership at its peak, over 35 percent of the private workforce by the mid-1950s, gave workers genuine bargaining power not just over wages but over the share of productivity growth that would flow to labor rather than to capital. Marginal tax rates above 90 percent for the highest earners made it structurally irrational to hoard wealth at the top rather than reinvest in wages and productive capacity. The Glass-Steagall Act passed in the 1930s directed capital toward productive investment rather than financial speculation.

Every one of these instruments was fought for against determined opposition. The business community resisted union power at every step. The financial industry chafed against regulation. None of it was natural. All of it was designed. And the design worked, for the specific population it included, precisely because it was predistributive. The result was a generation of genuine asset-builders rather than wage-earners watching prosperity compound upward without them.

The word that names what the post-war architects built without knowing they were building it is also the word that names what the New Deal could not fully deliver and what the shareholder revolution of the 1970s deliberately dismantled: ownership stakes in productive assets. By 1991, academic Michael Sherraden identified this as the structural challenge the New Deal fails to account for: income supports consumption; assets enable investment, stability, and mobility across generations. The welfare system's exclusive focus on income maintenance was not a partial solution to poverty. It was a system designed to manage poverty rather than end it, because it addressed the output of the ownership gap without touching the ownership gap itself.4

before wealth concentrates.

The Architecture of Exclusion

The post-war prosperity was real. It was also structurally bounded by design.

The GI Bill applied on paper to all veterans. In practice its wealth-building mechanisms were systematically withheld from Black veterans through a combination of legal architecture and deliberate administration. The Veterans Administration delegated implementation to local institutions which refused mortgage loans to Black applicants. The best-funded universities were segregated. The suburban developments built through FHA mortgage guarantees carried explicit racial covenants enforced by the federal government itself: the FHA's own underwriting manual rated neighborhoods with Black residents as high-risk and required racial homogeneity as a condition of loan guarantee. This was not private discrimination the government failed to prevent. It was discrimination the government designed and administered.

The structural consequence was not merely that Black families missed the post-war boom. It is that they were excluded from the mechanism by which the post-war boom compounded. A white working-class family that bought a house in a guaranteed suburb in 1948 did not simply enjoy prosperity in that decade. They participated in thirty, forty, fifty years of appreciation — equity that funded college tuitions, served as collateral for business loans, and transferred to the next generation as a head start that compounded again. Three generations of that compounding is what the wealth gap between white and Black households in America actually measures today. It is not primarily a wage phenomenon. It is not a cultural phenomenon. It is a compound interest problem, the direct output of a structural decision made in 1945 and running forward, uninterrupted, ever since.5

Post-war architecture proved that predistribution works and broad ownership distributed before concentration produces genuine and durable prosperity. It also proved that predistribution works only as broadly as the circle of inclusion is drawn. When the circle is deliberately narrowed, the mechanism still operates, it just operates for fewer people, and the exclusion compounds alongside the prosperity. The next architecture must draw the circle differently, not as an act of contrition but as the structural correction that honest accounting demands. An architecture that excludes by design is an architecture that reproduces the problem it claims to have solved.

The Break

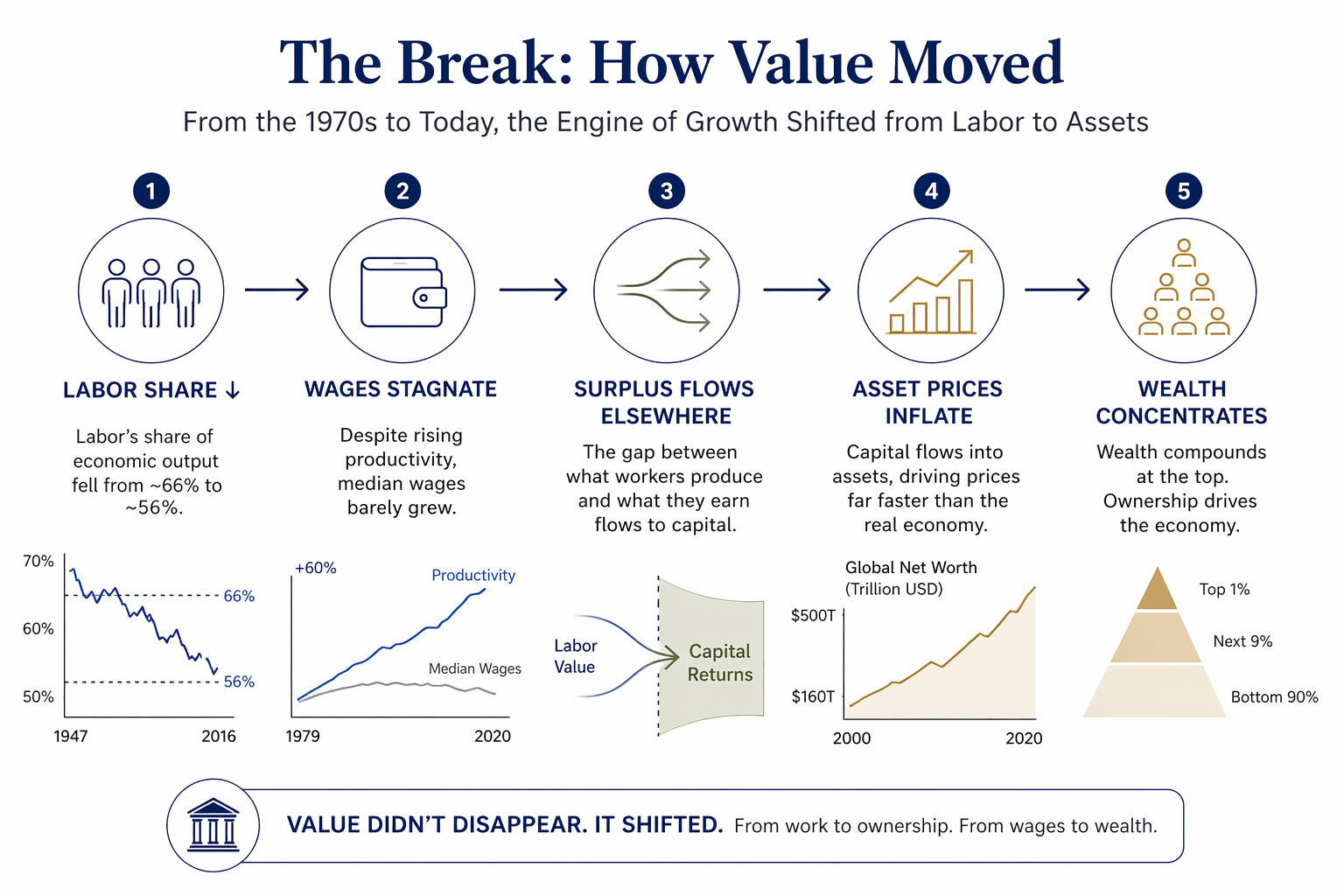

Productivity and wages, which had moved together for thirty years, diverged in the early 1970s and never reconverged. Productivity kept rising. Wages did not. The value that workers produced continued to compound, but it no longer compounded into paychecks. It compounded upward, into asset values, into equity, into returns on capital rather than returns on labor. Since 1979, productivity in the United States has risen by more than 60 percent. Median wages have risen by roughly 17 percent. The difference did not disappear. It was redirected.

That redirection is visible in a single shift. In the post-war decades, labor received roughly two-thirds of the value the economy produced. Today, it receives closer to three-fifths. That ten-point shift is not abstract. It represents trillions of dollars per year moving away from wages and toward profits, capital returns, and asset holders. What workers lost as income did not vanish. It accumulated elsewhere.

For decades, that shift could be debated. Today, it can be measured directly. Between 2000 and 2020, global net worth increased from $160 trillion to over $500 trillion, while global GDP grew far more slowly. The world did not produce three times more goods and services. Instead, the value of what already existed, homes, land, equities, financial assets, was repriced upward. Nearly 80 percent of that increase came not from new investment but from rising asset prices.

And the people who benefited are a narrow slice of the population. In the United States, the top 10 percent of households owned 71 percent of the nation's wealth by 2019, up from 67 percent in 2000. The bottom 50 percent owned 1.5 percent, down from 1.8 percent. Asset inflation is not broadly distributed prosperity. It is a transfer mechanism from those who hold assets to those who hold more of them, with roughly half the population holding almost nothing that appreciates.

This is the missing link. The stagnation of wages and the explosion of wealth are not separate phenomena. They are the same phenomenon viewed from opposite sides of the balance sheet. When labor's share declines, the surplus does not disappear. It flows into profits. When profits accumulate, they are reinvested into assets. When capital chases assets faster than the real economy grows, asset prices rise. And when asset prices rise, wealth concentrates in the hands of those who already own them. This is not a distortion of the system. It is the system operating as designed.7

By the early 1970s, the post-war architecture was under strain. Stagflation exposed the limits of Keynesian demand management. Regulated industries had become inefficient and captured by insiders. Unions, at their worst, protected incumbents without delivering corresponding productivity. The critique that incentives matter, that capital must be allowed to move, that markets allocate resources more efficiently than rigid systems, was not wrong. What followed, however, was not a recalibration. It was a reorientation of the system's objective function.

Milton Friedman's 1970 declaration that the sole responsibility of business is to increase shareholder value was not a description. It was an instruction. Corporate America followed it with precision. Returns to capital became the organizing principle of the economy. Reagan's dismissal of the air traffic controllers in 1981 signaled that labor would no longer have institutional protection at the highest level, and union membership began a decline from which it has never recovered. Financial deregulation, culminating in the repeal of Glass-Steagall, redirected capital away from productive investment and toward financial assets. Finance expanded from a supporting function into a dominant sector, growing from roughly 2.5 percent of GDP in 1945 to more than 8 percent by 2020.8

These changes did not fail. They succeeded on their own terms. Capital became more mobile. Markets became more efficient. Technology advanced rapidly. The problem is that the system that replaced the post-war model had no mechanism to distribute ownership alongside participation. Thomas Piketty formalized the result mathematically: when the rate of return on capital exceeds the rate of economic growth, wealth concentrates. The post-war period suppressed that dynamic through a specific set of institutions, strong labor participation, progressive taxation, regulated capital flows, and broad-based access to ownership. When those structures were removed, the underlying arithmetic reasserted itself.9

This is why wages are not coming back. Wages are tied to labor. Labor is no longer the primary driver of value capture. Ownership is. As long as the system channels gains into assets rather than income, growth will continue to show up in balance sheets, not paychecks. The economy can expand, technology can advance, productivity can rise, and the distribution mechanism will still channel the gains upward. Social insurance systems funded by taxes on wages, in an economy where wealth has migrated decisively to assets, face an arithmetic they cannot solve. As the population ages and the ratio of workers to retirees declines, that mismatch becomes unsustainable. The system was designed for a wage economy. It is now operating inside an asset economy.

The break is not that growth stopped. It is that growth changed form. And until ownership is addressed directly, the results will continue to concentrate, no matter how much the economy produces.

It is that growth changed form.

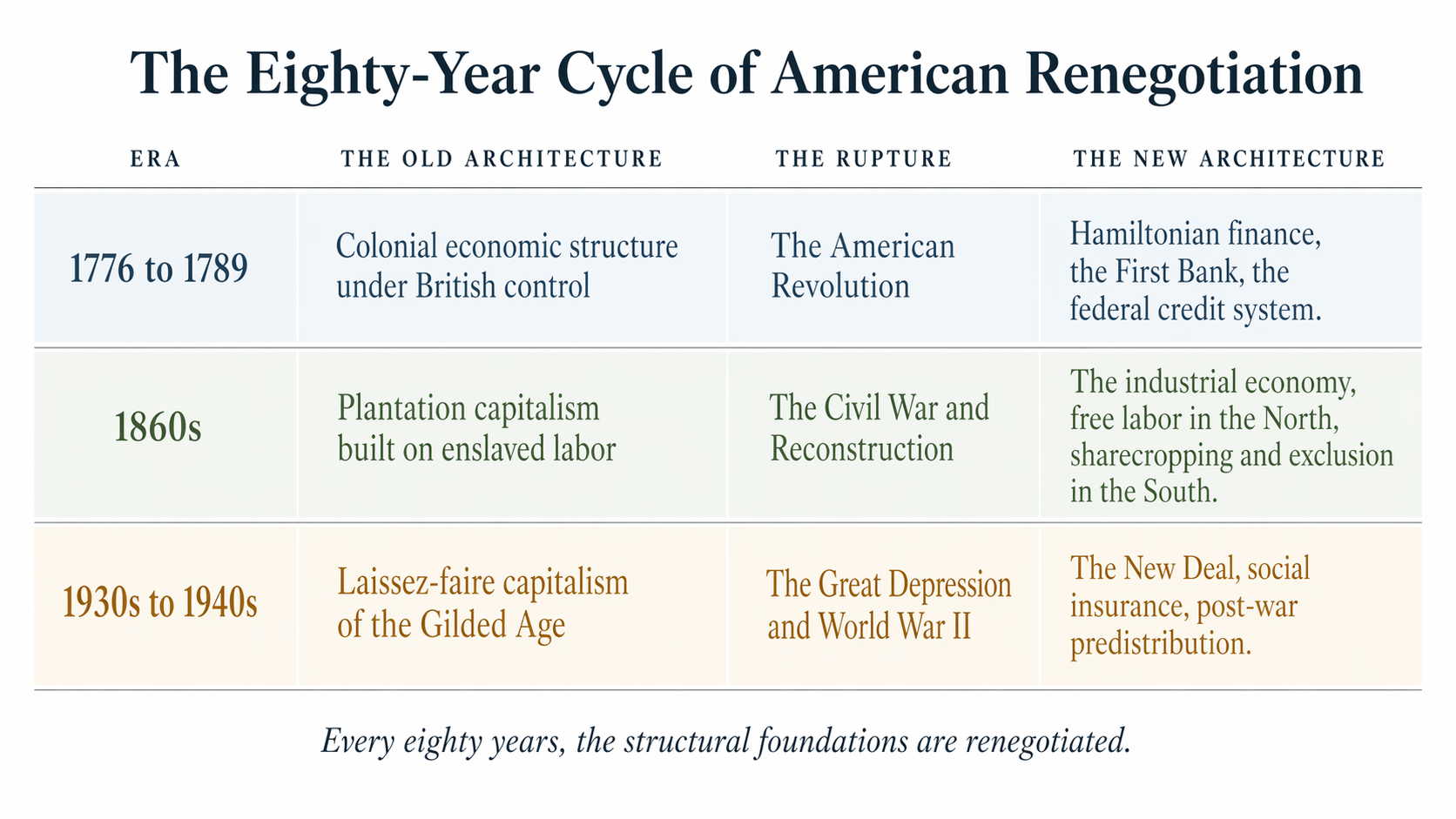

The 80-Year Cycle

Every eighty years, roughly, the structural foundations of American capitalism are renegotiated. The basic terms of who owns what, who governs the mechanisms of wealth creation, and on whose behalf the economy is organized are renegotiated at the foundation.

1776 to 1789: the Revolution broke the colonial economic structure. Hamilton's architecture replaced it. A new nation, a new financial system, new terms for who could participate in the economy and under what conditions.

The 1860s: the Civil War destroyed the plantation economy, the foundational structure of American capitalism in the South, the system that had made both North and South wealthy on the labor of people it treated as property. The Reconstruction amendments attempted, however incompletely and however brutally suppressed, to rewrite the terms of participation for four million people who had been held as capital rather than recognized as contributors. That attempt failed. The architecture that replaced it was sharecropping, convict leasing, the systematic exclusion of Black Americans from the wealth-building mechanisms of the industrial economy. It was a renegotiation in the wrong direction. But the old architecture could not survive the contradiction that had destroyed it, and from those ruins the United States built the largest industrial economy the world had yet seen.

The 1930s and 1940s: the Great Depression demolished the laissez-faire consensus of the Gilded Age. The New Deal rewrote the basic relationship between the federal government, capital, and labor. Then came the war, and from it the post-war architecture described above, the thirty-year window when the predistributive instruments briefly held and the American Dream was measurably within reach of working people.

It changes either way.

The question is who is in the room when it does.

We are eighty years from the New Deal. Wages have decoupled from productivity for fifty years, the institutions built to redistribute opportunity are fiscally strained and politically contested, and the Social Security Trust Fund faces structural insolvency within a decade. The revenue model of our social safety net was designed for a demographic pyramid that no longer exists, funded by a wage base that no longer captures where the wealth lives. Addressing today's challenges with yesterday's approach is the reason for our deepening political divisions: we are pointing fingers at one another instead of looking at the structures that can no longer serve their purpose. Artificial intelligence is compressing the timeline further, concentrating economic power at a speed and scale the old architecture was never built to govern. The question is not whether the architecture changes. It changes either way. The question is who is in the room when it does.

The Commons Has a Balance Sheet

The pattern of productivity compounding upward into asset values while wages stagnated, the predistributive architecture dismantled, the redistributive tools strained past their design limits is one instance of a longer pattern. What happened to wages between 1975 and 2020 is what has happened, repeatedly, whenever capital has identified a productive commons it could enclose, privatize, and extract without compensating the people whose labor and contribution made the commons productive in the first place.

The English enclosures of the sixteenth through nineteenth centuries were the first industrial-scale run of this pattern: common land on which generations of farmers had worked, grazed, and gathered was converted, through acts of Parliament and private power, into private property. The displaced peasants became wage laborers. The landed gentry became the owners of what had been held in common. The commons was productive and it was unowned. Capital identified the productivity, privatized the asset, and captured the return. The people whose labor made the commons productive received wages if they were lucky and nothing when the relationship ended.

That logic has run through every chapter of the American economy this Declaration has traced. The plantation economy ran it on human beings. The industrial economy ran it on labor.11 The platform economy runs it on something larger and more fundamental: the entire substrate of collective human production, the commons of care, knowledge, relationship, culture, and civic life on which every formal economic transaction ultimately depends. What is happening now with artificial intelligence is not a new chapter in that story. It is the same story, running at civilizational scale and software speed, with a new target: not a specific asset class, but the conditions of production themselves.

The Tool Is Inevitable. The Ownership Is Not.

Artificial intelligence substitutes for cognitive labor. Robotics substitutes for physical labor. Together, they are the productive infrastructure of the twenty-first century, and their deployment is not optional. The demographic arithmetic of every advanced economy requires them. Populations are aging, from Japan and China to Spain and Italy to the United States. Birthrates are below replacement across every industrialized society, because the expense of raising and educating children into their mid-twenties has moved reproduction from a net asset to a liability.12 Raising a family in the twenty-first century is not going to get cheaper. As the Baby Boomers fully retire, the workforce that built the twentieth century is contracting, and the care economy, the manufacturing economy, the service economy, and the knowledge economy cannot be sustained at their current scale without the productive augmentation these tools provide. Resistance may be a personal choice, but it is not an available position for businesses or national economies. The tools are being built, and they will be integrated across every sector of the economy in our lifetimes. The only remaining question is who owns what they produce.

The argument this Declaration makes is not against the technology. It is against the default ownership architecture under which the technology is being built.

It is against the default ownership architecture

under which the technology is being built.

The distinction is not rhetorical. The same tools deployed under two different ownership structures produce two different societies. Under the first, AI models and robotic infrastructure are owned by a small number of private entities that captured the commons before governance frameworks existed to protect it; the returns from every productivity gain the tools generate flow to the asset holders; the workers displaced by automation receive nothing from the value their replacement creates; the communities whose knowledge trained the models hold no stake in the infrastructure their contribution made possible. Under the second, the same tools are built on a commons whose ownership is distributed by contribution; the communities whose collective intellectual and cultural output trained the models hold a stake in the models; the productivity gains compound outward rather than upward. The tools are the same. The outputs are the same. The ownership of the tools, and therefore the distribution of what the tools produce, is different. That is the variable currently being decided.

The argument for distributed ownership is not coming only from outside the AI industry. Mustafa Suleyman, cofounder of DeepMind and CEO of Microsoft AI, has written that the program required to make frontier technology safe for human civilization is not resistance but containment: a balance of power not between competing actors but between humans and the tools themselves. In his account, containment requires four things: regulation, technical safety, new governance and ownership models, and new modes of accountability and transparency. He names ownership explicitly as one of the four necessary precursors. This is not the position of a critic writing from outside the building. This is the position of one of the handful of people on Earth actually building frontier AI systems, arguing that the default ownership architecture is insufficient for the scale of what is being built.13

The contrary position, also articulated from inside the industry, is most cleanly stated in Leopold Aschenbrenner's Situational Awareness, a document published in June 2024 by a former OpenAI researcher that has since shaped significant policy conversation. Aschenbrenner's argument is that superintelligence is imminent, that the coming decade will require a trillion dollars of capital and compute infrastructure at a hundred thousand times current scale, and that the United States must win this race against China at any cost through a Manhattan Project–style mobilization coordinated between the national security apparatus and a small number of frontier AI labs. Take the argument at its word. Assume the stakes are as he describes them. The governance architecture he proposes — concentrated, elite-led, national-security-framed, with guardrails set by the same actors building the technology — is a precise description of what the American political tradition has always recognized as the conditions under which concentrated power becomes unaccountable.14

The Declaration takes neither a utopian nor an apocalyptic view of the AI and robotics transition. The technology is being built, at speed, for reasons that are structural rather than ideological. Some of what is being promised will prove real. Some will prove to be the inflated valuations of an investment cycle requiring trillion-dollar flows to sustain itself. That uncertainty does not change the ownership argument. Whether superintelligence arrives in 2027 or 2047, whether the productive gains are as transformative as Aschenbrenner describes or substantially less, the ownership of the infrastructure being built right now will compound across generations. Concentrated ownership will produce concentrated returns. Distributed ownership will produce distributed returns. The tools are inevitable, but the ownership architecture is a choice.

The ownership is not.

The Commons We Have Not Named

Every economy runs on two kinds of input. The first is visible, measurable, and compensated: the labor that appears on a payroll, the capital that appears on a balance sheet, the intellectual property recorded in a patent filing. The second is invisible, unmeasured, and uncompensated: the substrate beneath every visible transaction, the collective human production that makes economic activity possible and that formal accounting systems were never designed to see.

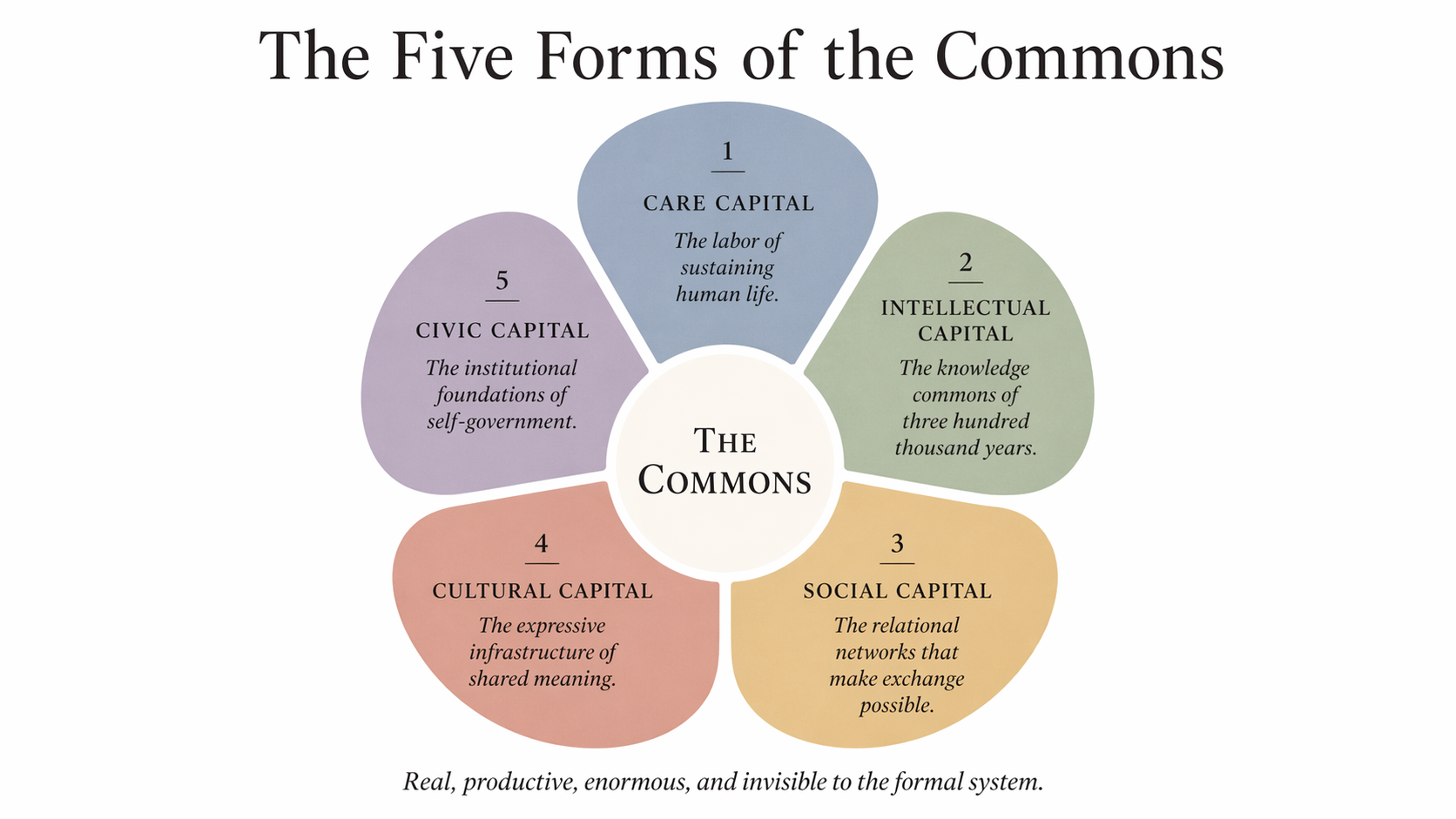

This substrate is not a single thing. It is at least five distinct asset classes, each productive, each collectively generated, each currently being extracted without compensation to the people who produced it.

The first is care capital — the labor of sustaining human life: feeding, healing, raising children, supporting the aged and the ill. It is the most essential labor in any economy and the least compensated. It is invisible to formal accounting because it resists enclosure: you cannot standardize care the way you can standardize a manufactured unit, you cannot make it excludable without destroying what makes it valuable, and its returns compound in ways that appear in public health outcomes and workforce productivity decades later rather than on any quarterly balance sheet. Every enterprise depends on a workforce that was raised, educated, fed, and cared for by labor that appeared on no one's books. That labor was not free. It was unaccounted.15

The second is intellectual capital — the knowledge commons. Three hundred thousand years of accumulated human thought: every scientific discovery built on prior discovery, every argument worked out in language developed over millennia, every technical innovation standing on a foundation of publicly funded research and openly shared knowledge. Individual contributions to it are real and traceable. Compensation for those contributions is essentially zero. The mathematical foundations underlying modern AI were developed in publicly funded universities. The linguistic structures that make large language models possible were produced by the entire human species across all of recorded history. None of the contributors hold a stake in the infrastructure their contribution made possible.16

The third is social capital — the relational commons. Robert Putnam spent decades documenting what economists had systematically failed to measure: that the density of networks, norms of reciprocity, and relationships of trust within and across communities is a productive asset that generates real economic returns. He distinguished bonding capital, the dense ties within communities that provide security and enable collective action, from bridging capital, the connections across communities that enable economic mobility and make transactions between strangers possible. Both forms are productive. Neither appears on any balance sheet. Both are being systematically extracted.17

The fourth is cultural capital — the expressive commons. Language itself. Story, music, artistic form, the shared symbols and meaning-making frameworks through which a community understands itself and transmits knowledge across generations. This is not the same as intellectual capital, though they overlap. Cultural capital is the medium in which intellectual capital circulates, the shared expressive infrastructure without which knowledge cannot be accumulated, transmitted, or built upon. It is produced collectively, across generations, through the uncompensated creative work of every person who has ever contributed to a living culture. It is currently being absorbed into AI training sets at a rate that makes individual attribution impossible. Collective compensation, under existing legal frameworks, is unimaginable.18

The fifth is civic and institutional capital — the governance commons. The accumulated work of building and maintaining the public institutions, legal frameworks, democratic norms, and governance structures that make a functioning economy possible. Rule of law. Contract enforcement. Public health infrastructure. Educational systems. The regulatory architecture that makes financial markets trustworthy enough to function. None of these emerge from markets. They are produced by collective human effort across generations, maintained by ongoing civic labor that is largely uncompensated, and treated as free inputs by every private enterprise that depends on them. When they degrade, when civic capital is depleted by the same extraction logic that depletes every other commons, the formal economy loses the substrate it requires without registering the loss until the failure is catastrophic.19

The formal economy is extraordinarily skilled at measuring what capital can price, and capital prices what can be made excludable, transferable, and tradeable. What resists enclosure gets systematically undervalued. The work that most resists enclosure: care, teaching, organizing, the relational labor that makes trust possible and therefore makes commerce possible is the least compensated, least protected, and least visible work in the system. The work most compatible with enclosure: financial engineering, platform architecture, the management of already-concentrated capital is the most compensated, most visible, and most protected. The economy does not get the hierarchy of value wrong by accident. It gets it wrong by design: a design optimized for enclosure, structurally blind to everything enclosure cannot reach.

Hernando De Soto spent decades documenting one dimension of this problem. Traveling through the developing world, he found something that overturned the conventional narrative about poverty: the poor are not poor because they lack assets. They possess enormous assets including informal housing, small businesses, community networks, accumulated knowledge and skill built over lifetimes. What they lack is the legal and institutional infrastructure that converts those assets into capital. Clear title. Enforceable contracts. Formal records. Access to credit markets. Without that infrastructure, the assets are what De Soto called dead capital, real value that cannot be activated, cannot be leveraged, cannot compound. Present but inert.20

The same insight extends to every dimension of the commons. The care worker's twenty years of patient knowledge, the teacher's curriculum, the organizer's network, the scientist's publicly funded research, all of it dead capital, in De Soto's sense: real, enormous, productive, and invisible to the formal system because no institutional architecture has been built to make it legible to the people who produced it.

What cannot be protected will be enclosed.

GDP is not a measure of what was created. It is a measure of what was credited. The gap between those two things, between the full account of what produced value and the narrow account of what received recognition, is this Declaration's operating definition of the problem it is solving. And that gap has never been wider or more consequential than it is right now, as the largest act of commons extraction in human history runs at software speed through every sector of the economy simultaneously.

The Extraction Architecture

The platform economy of the twenty-first century discovered that all five asset classes can be monetized simultaneously through a single architecture. The platform provides a technical interface. Users bring their care relationships, their intellectual output, their social networks, their cultural production, and their civic participation to that interface. The platform captures the data generated by all five, converts it into behavioral prediction products and targeted advertising inventory, and returns nothing to the contributors. The platform does not produce any of the underlying value. It produces the enclosure mechanism, the institutional infrastructure that makes the previously invisible commons legible to capital. It is De Soto's insight inverted: instead of making the commons legible to the people who produced it, it makes the commons legible to whoever owns the platform.

Jaron Lanier identified the structural logic a decade ago. Writing about what he called siren servers, he described platforms whose entire value derived from the collective intelligence and social behavior of their users and which returned nothing to the people whose contributions created that value.21 What he described for social media has now been generalized to every dimension of collective human production simultaneously. Social media extracted the attention, behavioral data, and social capital of billions of living people. Large language models have extracted the intellectual and cultural output of the entire species across all of recorded history. The scale is not comparable in degree. It is different in kind.

Shoshana Zuboff named the governing logic: surveillance capitalism, an economic form in which human experience itself is claimed as raw material for the production of behavioral prediction products sold without the knowledge or consent of the people whose lives generated them.22 Her framework makes visible what GDP cannot measure: the extraction is not incidental to the business model. It is the business model. The platform does not sell a product to its users. It sells its users, their attention, their relationships, their behavioral patterns, their cultural output, their civic participation, to whoever will pay for the predictive power that data generates.

It sells its users — their attention, their relationships,

their behavioral patterns, their cultural output, their civic participation —

to whoever will pay for the predictive power that data generates.

This is why the standard antitrust response to platform monopoly is structurally insufficient. Breaking up a platform addresses market concentration within a single asset class. The platform monopoly operates across all five commons simultaneously. Its power derives not from controlling a specific market but from controlling the infrastructure through which the commons is converted into capital. The problem is not the size of the platforms. It is the architecture of enclosure they represent, and that architecture will reassert itself in any successor platform built on the same ownership logic.

The Final Enclosure

Artificial intelligence concentrates this extraction at a scale that requires a different category of response. The difference is not in the value of the tools. The difference is in what has been absorbed to make them work.

The large language models now foundational to the global economy were trained on the accumulated written output of human civilization: every book that survived long enough to be digitized, every article, every argument, every lesson, every story across every culture and every century. The contributors to that commons number in the billions across all of recorded history. Their collective intellectual and cultural labor created the substrate on which these systems run. They were not asked. They were not compensated. They own nothing of what their contribution made possible. The entire human knowledge commons of every teacher, every scientist, every writer, every storyteller who ever lived has been absorbed into private infrastructure generating returns for a small number of people who arrived at the table with capital at the precise moment the technical capability to perform the absorption became available.

The economic implications are already visible and will accelerate. The Magnificent Seven technology companies — Apple, Microsoft, NVIDIA, Amazon, Alphabet, Meta, Tesla — have driven the majority of equity market returns over the past decade. Their combined market power reflects something the standard concentration metrics do not capture: they are not merely large companies in large markets. They are the owners of the enclosure infrastructure through which the five commons are being converted into private capital. The gains are accruing to asset holders at a rate that makes the post-war productivity-wage divergence look gradual. AI systems increasingly substitute for both cognitive and physical tasks. Wealth accrues to those who own the platforms and the infrastructure. The workers and communities whose knowledge, care, relationships, culture, and civic labor made those systems possible receive nothing from the assets their contribution helped create.

This is not a technology story. It is an ownership story. The tools will be built regardless of how the ownership question is answered. Whoever owns the infrastructure of the enclosure owns the returns from everything the commons produces, and the question of who owns that infrastructure is being decided right now, by a small number of people, with consequences that will compound across generations.

Separation of Powers

The American political tradition has confronted a version of this problem before. In 1787, the framers faced a structural question not unlike the one this Declaration is raising: how do you build an architecture that can hold power without being captured by it? Their answer was not to trust the virtue of any particular person, party, or institution. It was to distribute power across competing branches and levels, to design checks and balances that made concentration irrational rather than merely inadvisable, and to write those distributions into a founding document that no single actor, however popular, however urgent their cause, however compelling their case, could unilaterally overturn.

The architecture worked. Not perfectly, not continuously, not without failures that required centuries of correction. But it worked in the one respect that mattered most: no individual, no faction, no branch of government has been able to accumulate enough power to end the experiment. Presidents overreached. Congresses abused authority. Courts imposed ideology. Parties captured machinery. In every case, the structure provided a mechanism for correction because no single node in the system could disable the others. Two hundred and fifty years is a long time for a political system to hold together in the face of civil war, economic collapse, demagoguery, and technological transformation. It has held because it was designed for distributed power.

No equivalent architecture exists for economic power. The Hamilton-Jefferson debate was about how to govern concentrated ownership, not about whether ownership itself should be distributed. The post-war settlement used redistribution to manage the outputs of concentration without addressing the structure of concentration itself. The platform economy has accelerated concentration at a speed and scale that no redistributive instrument can match. The AI and robotics transition, already underway, is compressing the timeline further.

What the framers did for political power is what the twenty-first century requires for economic power: a structural distribution of ownership and governance across the infrastructure being built right now, written into founding instruments that no subsequent actor can unilaterally overturn. Not because the people building the technology are untrustworthy, but because concentration, once it sets, becomes the architecture that we all build upon. The only discipline durable enough to resist capture is the discipline that refuses to rely on the virtue of whoever happens to hold power at any given moment.

The tools are a given. The architecture is a choice. The people most affected by that choice are not in the room where it is being made.

Every generation that has inherited this republic

has faced some version of the same question:

the institutions built by the previous generation were adequate for the world they lived in

and are no longer adequate for the world that has arrived.

The United States has been here before. Every generation that has inherited this republic has faced some version of the same question: the institutions built by the previous generation were adequate for the world they lived in and are no longer adequate for the world that has arrived. The generation that wrote the Constitution replaced the Articles of Confederation because the Articles could not hold thirteen states together against the centrifugal forces of the new economy. The generation of Lincoln dismantled the slave economy that the founders had deferred resolving, and rebuilt the republic on a foundation the founders had been unwilling to lay. The generation of Theodore Roosevelt and Woodrow Wilson built the regulatory state to govern an industrial economy the framers could not have imagined. The generation of Franklin Roosevelt built the social insurance architecture that made mass prosperity possible for seventy years and that is now, by its own design, reaching the limits of what it can carry. None of those generations inherited an economy they could leave untouched. Each had to take what had been passed to them, assess what still worked, and rebuild what did not.

That is the inheritance, and that is the obligation. The institutions we were given were built by people who understood that the work of passing a functioning republic to the next generation is not preservation. It is reinvention. The question Section IV takes up is which institutions of the twentieth century can carry us forward, which cannot, and what the next architecture has to look like if the productive capacity of the twenty-first-century economy is to be held broadly enough to sustain the democratic commitments the previous architectures were built to protect.

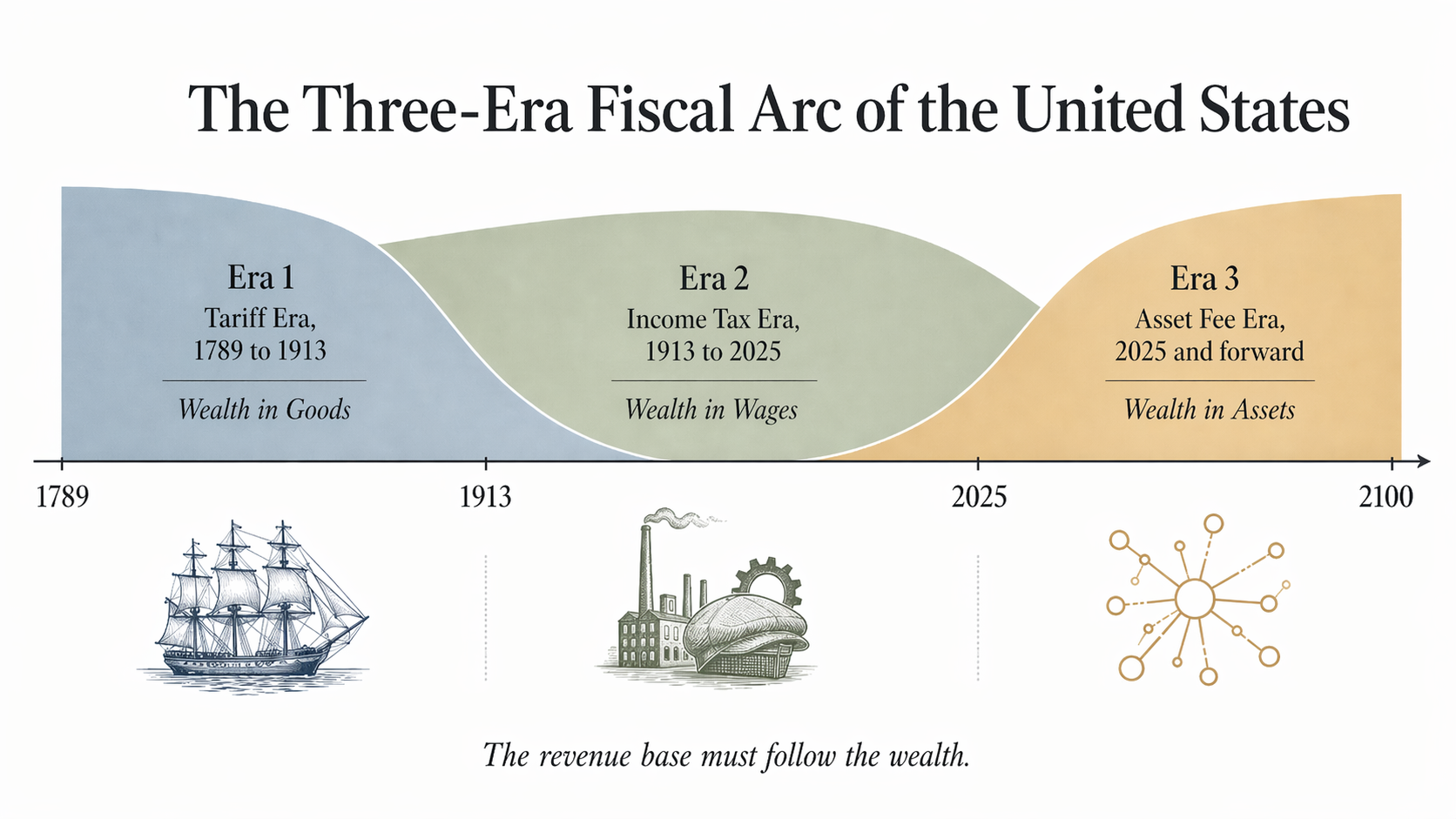

The Three-Era Fiscal Arc

The New Deal was the most successful redistributive architecture in American history. In the wreckage of the Great Depression, a quarter of the workforce unemployed, banks failing by the hundreds, democracy fracturing at the edges, a set of institutional innovations did something that had never been done at scale in a modern industrial economy. It stabilized a society that was genuinely coming apart. Social Security. Unemployment insurance. The FDIC. The Wagner Act. The regulatory architecture that governed finance for a generation. For thirty years, in combination with the predistributive instruments described in Section II, these institutions produced something genuinely resembling shared prosperity. The extremes of wealth and poverty were narrowed and the middle class expanded. America became a symbol of democracy and the economic engine of the world at a time when totalitarianism and communism were the competing worldviews.23

The problem is not that the New Deal failed. The problem is that it succeeded at a specific task, redistribution, and we have spent seventy years asking it to accomplish a different task its architecture was never designed to perform. Redistribution corrects concentration after it happens. It does not change who participates in ownership before it happens. A Social Security check does not compound and does not appreciate. Medicare pays for care, but does not create a stake in the care enterprise. Unemployment insurance bridges a gap, but does not close it. Every redistributive instrument in the New Deal toolkit is designed for income replacement, not for changing the ownership structure itself. The citizen in the redistributive model remains structurally a recipient.

The New Deal was not a theory. It was triage. When the patient is bleeding, you apply pressure. You do not stop to redesign the circulatory system. But triage is not a long-term health strategy. Redistribution applied across decades as permanent architecture rather than emergency intervention reveals its structural ceiling. You cannot redistribute your way to an ownership society. You can only redistribute your way to a slightly less unequal non-ownership society, and only for as long as the fiscal conditions that make redistribution possible hold.24

The Three-Era Fiscal Arc

Those conditions are no longer holding. There is a divergence between where the wealth lives and where the revenue base is pointed, and it has been widening for fifty years.

The revenue base of any government must follow the wealth of the economy it governs. The tariff was the principal funding mechanism of the United States for the first 150 years of its existence, because the movement of physical goods in an agrarian and manufacturing economy was the basis of wealth building. When the wealth moved to wages, the revenue base followed. The 16th Amendment established the income tax in 1913, funding the most expansive social insurance system in American history from the wages of a manufacturing, employment-based economy. Both transitions were fought for, contested, and eventually ratified, because the alternative was a government that could no longer govern.

The wealth has moved again. Fifty trillion dollars sit in American retirement accounts alone. The top ten percent of households own seventy percent of all financial assets. The bottom fifty percent own two and a half percent. Corporate equities, real estate, intellectual property, platform infrastructure: the productive capacity of the American economy is organized around ownership now, not around wages. Compounding returns flow to those who hold assets, not to those who sell their labor. And the social insurance system, built on the assumption of a growing wage base, funded by a tax on the thing that is no longer where the wealth primarily lives, faces structural insolvency within a decade.25

This is the Three-Era Fiscal Arc. The tariff era. The income tax era. The Asset Fee Era, which is not coming. It is already beginning, in the form of wealth tax proposals, data levy discussions, AI infrastructure debates, and the growing recognition across the political spectrum that the income tax base cannot sustain the social insurance commitments the country has made. The question is not whether the revenue base shifts toward assets. It will shift. The only question that is actually ours to answer is whether the shift is designed to serve everyone, or designed to serve the people who already hold the assets.

Redistribution applied to the Asset Fee Era produces a larger, more aggressive transfer machine. Better than letting the income tax era collapse without replacement, but insufficient as a permanent architecture, because it does not change the underlying ownership structure. Predistribution applied to the Asset Fee Era produces a different economy: one in which the productive capacity of the asset economy is broadly held before it concentrates, one in which the people who contribute to building the commons hold a stake in what the commons produces, one in which the question of redistribution becomes less urgent because the question of concentration never fully arose.

These are not the same project. They do not produce the same society. The choice between them is being made now, in the decisions of this decade, in the same way the choice between the tariff era and the income tax era was made by a specific generation of legislators, economists, and reformers who recognized that the old revenue base could no longer fund the obligations of the early twentieth century.26 The Asset Fee Era arrives first in one sector, at a scale that forces every other fiscal question into its shadow, and in a form the redistributive architecture was never designed to govern.

Healthcare and the Arithmetic of the Commons

Healthcare is already the largest sector of the American economy. National health expenditures reached $4.9 trillion in 2023, 17.6 percent of GDP, larger than defense, larger than education, larger than any other category of human activity the country records. It is not a vertical alongside other verticals. It is the spine of the social sector, the place where demography, labor, technology, and fiscal policy converge, and the first system in the American economy where the twentieth-century redistributive model arithmetically stops working.27

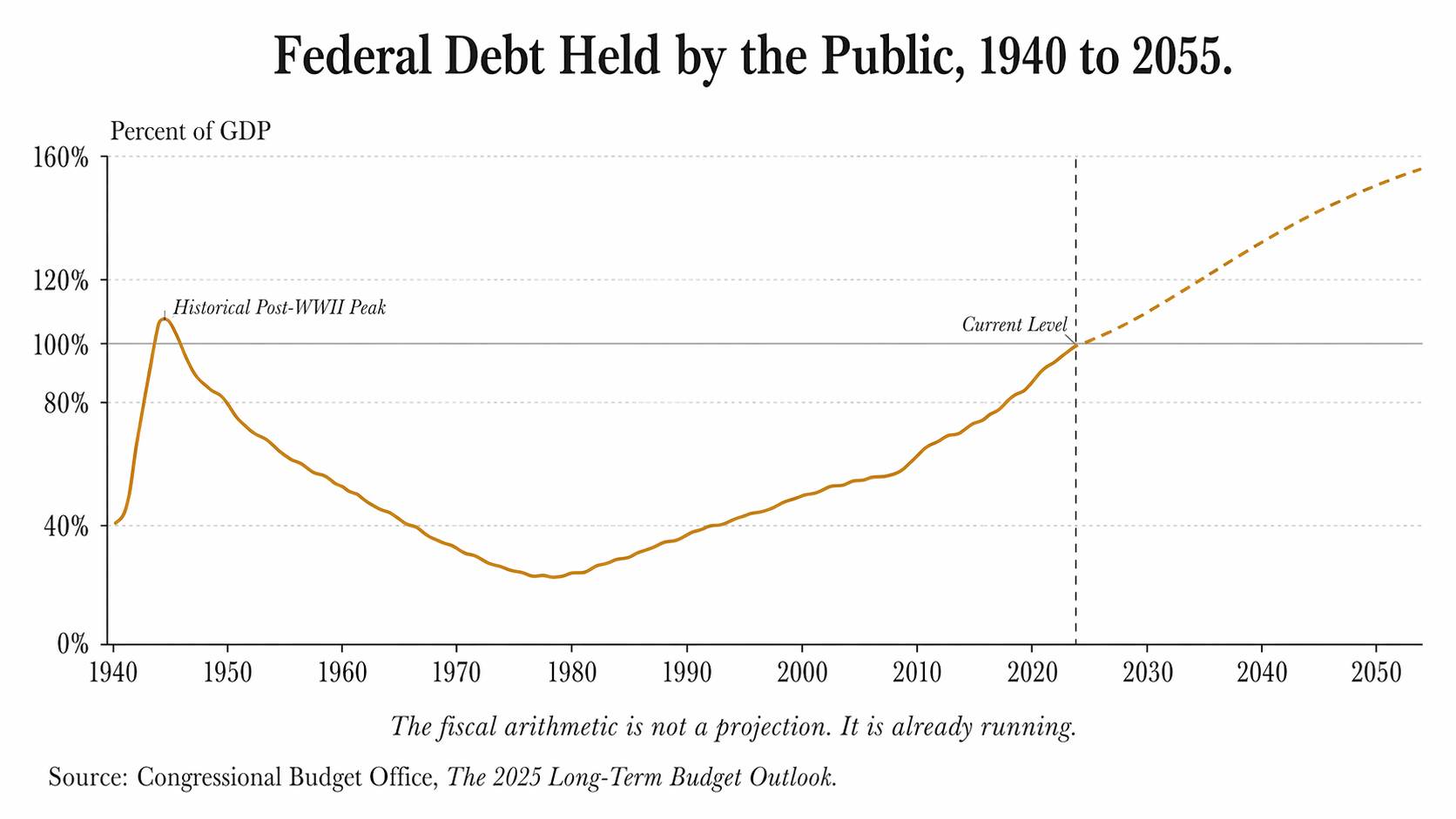

The forces driving that arrival are structural and irreversible. The population is aging. Life expectancy has extended. The old-age dependency ratio, 37 seniors per 100 working-age adults today, rises to 46 per 100 by the 2050s. Care work is labor-intensive, locally delivered, and only partially substitutable by technology. The wage base that funds social insurance is being compressed by AI and automation in the sectors where labor can be replaced, even as demand rises fastest in the one sector where it cannot. The fiscal arithmetic follows directly. Federal debt held by the public is roughly 100 percent of GDP today. Under current law, by 2055 it reaches 156 percent, driven by the compounding interaction of an aging population, healthcare cost growth above general inflation, and interest payments on existing debt. Spending on Social Security, major federal health programs, and net interest rises from 14.2 percent of GDP in 2025 to 19.6 percent by 2055, while revenues rise only 2.2 points over the same period. The gap between those trajectories is not a projection. It is a design mismatch. The system is not failing because it is mismanaged. It is failing because it is correctly designed for conditions that no longer exist.28

This is why redistribution alone cannot close the gap. Healthcare is where the old model breaks first because it is where demographic inversion, labor that resists automation, and a shrinking tax base compressed by automation everywhere else converge in the same sector at the same time. AI substitutes for cognitive labor. Robotics substitutes for physical labor. Together they compress the wage base that funded the twentieth-century social contract from both ends simultaneously, and the arithmetic of that compression is no longer a projection. It is the trajectory the capital has already chosen.29

The revenue base must follow the wealth, into assets, into data, into the returns from the infrastructure that increasingly produces the economy's output, because the wage base it used to follow is no longer where the wealth lives.

The Compounding Logic and Who It Serves

The compounding logic at the center of the American economic engine is the structural answer to this convergence, the mechanism by which contribution, held patiently over time, builds the stake that no redistributive transfer ever can. It is also the oldest argument in the American economy, made repeatedly across three generations of practitioners and thinkers who arrived at the same structural conclusion from different directions: Kelso from first principles, Buffett from six decades of practice, Thiel from the architecture of platform monopoly. The mechanism works. It has always worked. The only question left is who it works for.

Louis Kelso saw it first, in 1958, not from historical data but from the internal logic of capitalism itself. If capital ownership decisively overtakes wage labor as the primary driver of wealth creation, he argued, the solution is not higher wages or redistribution but broader ownership, making the mechanism that compounds work for more people, not just the people who already hold assets. His invention, the Employee Stock Ownership Plan, was the first systematic American mechanism for converting labor contribution into ownership stake before the profits are generated rather than distributing income after the fact. It worked. There are thousands of ESOP companies in the United States, and they are on average more productive, more stable, and more equitable than their conventionally owned counterparts. The mechanism was real. But the ESOP has a ceiling that Kelso's century could not see past. It was designed for the industrial economy, for a world where the contributor is an employee, the enterprise is a firm with identifiable physical assets, and the ownership stake can be formalized within the structure of employment. The knowledge economy breaks all three conditions. The teacher whose thirty years of curriculum innovation is absorbed into an AI training set is not an employee of the company that trained the model. The care worker whose institutional knowledge is the actual product of the care relationship owns nothing of the enterprise that depends on her staying. The ESOP is the right answer applied to the wrong century. It pointed toward the principle without being able to complete it.30

Warren Buffett proved the principle at a scale Kelso never reached. Over six decades, through patient long-term investment in productive enterprises with genuine competitive advantages, businesses with durable moats, honest management, and predictable earnings, Berkshire Hathaway compounded capital at a rate that made it one of the most valuable enterprises in human history. The mechanism was not financial engineering. It was not speculation or extraction. It was ownership, held patiently, allowed to compound, trusted to generate returns over decades rather than quarters. Buffett demonstrated that the compounding logic of capital, applied with discipline and time, is the most powerful wealth-generating mechanism available, more powerful than wages, more powerful than redistribution, more powerful than any income-based strategy ever devised.

He also said something almost no one at his level of the ownership economy has been willing to say plainly: that he won what he called the ovarian lottery. Being born in America, in this century, with his particular aptitudes, in a system that rewards those aptitudes, accounts for the overwhelming majority of what he has accumulated. He has called the American institutional infrastructure, the rule of law, the financial architecture, the educated workforce, the social trust, the American Tailwind, and he has acknowledged that without it, his compounding logic would have had nothing to compound on. The argument of this Declaration is that Buffett is right about everything. Right about the power of the compounding mechanism. Right about the Tailwind that makes it possible. Right about the extraordinary productive capacity of the American economic engine. And he has not yet followed his own acknowledgment to its structural conclusion: that the Tailwind is a commons, that the commons requires governance, and that the people whose labor, care, and civic participation maintains it deserve the same compounding ownership stake that Buffett has spent his career building for those who arrived with capital.31

Buffett proved that the compounding mechanism, applied with patience and structural discipline, generates more durable value than any alternative. He left open the question of who owns the architecture that makes compounding possible. Thiel answered that question with uncomfortable precision.

Zero to One is, on its surface, a defense of corporate power. It is actually a theory of how transformative value gets created and how it compounds. Thiel argues that the goal of any serious builder is not to compete better but to escape competition entirely by creating something categorically new, and that durable value comes from building four characteristics into the foundation: proprietary technology that is qualitatively superior, network effects that compound with each additional user, economies of scale that drive marginal cost toward zero, and brand that makes alternatives feel wrong rather than merely inferior. The founding moment is the moment of maximum leverage, because the architectural decisions made at the founding determine the ceiling of what is possible for the life of the platform. Change the architecture later, and you are fighting the compounding you already set in motion.

The Declaration accepts Thiel's analysis of how compounding works entirely. The disagreement is not about the mechanism. It is about the ownership of the mechanism. The commons of human knowledge, care, relationship, and culture already has all four of Thiel's characteristics. It has proprietary depth that no competitor can replicate, three hundred thousand years of accumulated human thought. It has network effects, every additional contributor making it richer for every existing contributor. It has economies of scale, with the marginal cost of an additional person drawing on the shared intellectual and relational infrastructure approaching zero. And it has the deepest brand possible: it is the foundation of everything human civilization has ever built. What Google, Facebook, and the AI companies have done is precisely what Thiel prescribes: identify the most valuable unbuilt position, establish architectural dominance before competitors understand what is being built, and design the four characteristics into the foundation so the position compounds indefinitely. They did it correctly. What they built their monopoly on was the commons, and they built it so the compounding flows upward to the owners of the architecture rather than outward to the contributors who made it possible.

and they built it so the compounding flows upward

to the owners of the architecture

rather than outward to the contributors who made it possible.

The same architectural discipline, applied from the beginning with ownership designed to compound outward rather than upward, produces a different economy. Not because contributors are more virtuous than capital holders, but because the architecture can be designed that way, and once designed that way, it compounds that way for the life of the platform. You cannot monopolize abundance if abundance is the product of relationship. The architecture that captures relational and intellectual abundance must compound outward, which is not a departure from Thiel's logic but its completion, applied to a commons rather than a corporation.32

Predistribution in 2026

The instruments of 1945 are not the instruments of 2026. The GI Bill worked because a specific population, sixteen million returning veterans, met a specific asset class, housing in a specific window of appreciation, through a specific institutional infrastructure, the FHA, the VA, and the university system that could deliver the stake at scale before the post-war wealth concentrated. Those conditions are gone and the instruments must change, but the principle still holds.

Predistribution in 2026 looks like a care cooperative where workers earn ownership stakes in the enterprise their labor builds. It looks like a public semiconductor strategy where the public investment creates a public equity stake held in community wealth funds rather than dissolved into private balance sheets. It looks like an AI governance framework where the training data commons generates a collective ownership stake for the communities whose knowledge made the model possible, held in a structure that cannot be revoked when the political coalition changes or the corporate strategy shifts. Redistribution asks who gets the proceeds. Predistribution asks who owns the thing that produces them.33 Predistribution is a direction, not a blueprint. What follows is the set of principles that any architecture pointed in that direction must satisfy.

Predistribution asks who owns the thing that produces them.

What We Hold to Be True

The founders did not know what was coming. They could not have predicted industrialization, the transcontinental railroad, the telegraph, the rise of finance capital, two world wars, the collapse of empires, the civil rights movement, or the digital economy. What they did was something different and more durable: they named the structural shifts their generation had lived through, declared the principles that would govern the response, and built an architecture designed to hold under conditions they could not foresee.

We are in the same position now. We cannot predict the speed of artificial intelligence, the deployment timeline of humanoid robotics, the trajectory of great-power competition, the shape of the climate transition, or the political and social consequences of any of them. What we can do is name the shifts that have already arrived and state the principles that must govern the architecture we are about to build.

The Shifts Are Structural and They Are Not Reversible

From growth to contraction. The twentieth century was organized around population growth; the twenty-first will be organized around demographic contraction. Fewer workers support more retirees for longer lives in care-intensive years. The fiscal arithmetic of every advanced economy runs through that inversion first.

From wages to assets. The twentieth century distributed value through wages; the twenty-first distributes value through asset ownership. The productive capacity of the economy has moved from payrolls to platforms, from income streams to equity stakes, from the work people do to the infrastructure they work within. The revenue base of the state must follow the wealth or cease to function.

From machines to intelligent machines. The twentieth century's defining technology was the machine; the twenty-first's is the intelligent machine. Artificial intelligence substitutes for cognitive labor. Robotics substitutes for physical labor. The two waves together compress the wage base from the top of the knowledge economy downward and the bottom of the physical economy upward, and the returns flow to whoever owns the infrastructure that performs the substitution.

From redistribution to predistribution. The twentieth century's response to concentration was redistribution; the twenty-first's must be predistribution. Redistribution corrects outcomes after the concentration has occurred. Predistribution changes who participates in the concentration before it arrives. The New Deal was the most successful redistributive architecture in American history and it cannot carry the load the twenty-first century is placing on it. The difference is not a question of ideology. It is a matter of where wealth building occurs.

These are the shifts. They have already arrived. What follows is not a prediction. It is a declaration of what must be true of any economic architecture that intends to meet these shifts and preserve universal sovereignty. The principle that every person has a rightful stake in the productive capacity of the society they contribute to, and that the purpose of economic structure is to secure that stake rather than concentrate it.

If you hold universal sovereignty as a value, these eight principles are what the architecture requires. If you do not, and you believe sovereignty is properly distributed by market outcome, inherited position, technological advantage, or the accumulated returns of those who arrived with capital, you will build something else. That something else is what we already have.

Prosperity is a collective creation.

Entrepreneurs take risks that most people will not take, and when those risks produce something lasting, the reward is earned. But no one builds alone. The economy miscredits value at the point of creation. Returns go to the person at the visible top of the hierarchy, while the web of contribution that made the hierarchy possible goes unrecorded. The accounting was built to produce this outcome. The principle is the correction: credit contribution when it happens, not redistribute after the fact. Everyone who built something built it on a commons — on language developed across centuries, on infrastructure paid for by generations of taxpayers, on knowledge from ancestors who received nothing for it, on the trust that makes markets work and the care that raises the workforce without appearing on any balance sheet. The self-made individual is the story that extraction tells about itself.34

The commons has a balance sheet.

The care worker's twenty years of patient knowledge. The teacher's curriculum. The organizer's network. The scientist's publicly funded research. All of it is real, productive, and invisible to the formal economy because no one has built the system that would make it legible to the people who produced it. This is dead capital: present but inert, enormous but unrecognized. The pattern runs through all five forms of the human commons — care, knowledge, relationships, culture, and civic life. The commons needs a balance sheet not to privatize it but to give it legal standing, governance, and a way to return value to the people who built and maintain it. What cannot be measured cannot be protected. What cannot be protected will be enclosed.35

Contribution creates ownership.

Ownership produces what redistribution cannot: a genuine stake in what is being built, the alignment that makes care rather than extraction the rational choice, the compounding that turns contribution over time into something that lasts. This is not a moral claim. It is a structural one. Employee-owned companies outperform their conventionally owned counterparts not because employee-owners are more virtuous but because the architecture changes the relationship between contribution and return. Ownership here is not purchased. It is not granted. It is earned through verified work, recorded before the value concentrates, and made irrevocable once established. A stake earned this way compounds for the person who earned it, for the enterprise they helped build, and for the next generation that inherits the architecture.36

The protocol cannot be owned.

Any structure that can be owned can be captured. Any structure that can be captured eventually is because the pressure of concentrated ownership eventually overwhelms the commitments of the people who started it. The protocol layer is the commons of knowledge, care, relationships, culture, and civic life. It is governed by contribution, not owned by capital. Operating businesses built on top of the protocol can be owned, traded, and compounded with the full force of the market. That is where the energy and reward of private enterprise belong. But the foundation underneath them is the inheritance of everyone who contributed to it, and it cannot be acquired, sold, or revoked.37

The covenant must precede the capital.

Every major failure of broad ownership in American history has the same shape: the capital arrived before the covenant, and once the capital arrived with its own interests, the governance followed the capital. Reconstruction: the promise of forty acres and a mule revoked within a year of Lincoln's assassination because the architecture that would have made it irrevocable was never built before he died. The AI commons: enclosed before any governance existed to protect it, now far harder to restructure than it would have been to govern at the founding. The structural lesson is always the same. The rules must be written before the money arrives, before the interests diverge, before the people who made the commitments are no longer in the room.38

The engine must be regenerative by design.